Standard Deductions vs. Itemized Deductions: Which Should I Choose?

8 MIN READ | DEC 19, 2025

By

By

Link copied!

Unable to copy link. Please try again.

Key Takeaways

- Deductions reduce your taxable income, which could put you in a lower tax bracket and save you money.

- The standard deduction lowers your taxable income by a fixed dollar amount based on your filing status, age and several other factors. Itemized deductions, on the other hand, lower your taxable income based on certain expenses you paid during the tax year.

- Here are some itemized deductions that can lower your taxable income: mortgage interest, charitable donations, medical expenses, and state and local taxes—but there are limits and exceptions.

- For most people, the standard deduction is the easiest option and saves you the most money and time—but it doesn’t hurt to add up your potential itemized deductions because, depending on your situation, itemizing could save you even more.

The IRS gives you two ways to reduce your taxable income when you file your taxes. You can choose to take the standard deduction, or you can itemize your deductions.

Taking the standard deduction is as easy as ticking a box, while itemizing your deductions requires a fair bit of work and organization.

Like a lot of things involving the government, it can get complicated fast. The trick is figuring out which one will lower your taxable income the most.

What Is the Standard Deduction?

The standard deduction is a specified dollar amount you can subtract from your taxable income when you file your taxes. That amount—which the IRS decides every year—depends on your filing status and, in some cases, your age and several other factors.

|

Standard Deduction |

|||

|

Filing Status |

2024 |

2025 |

2026 |

|

Single |

$14,600 |

$15,750 |

$16,100 |

|

Married Filing Jointly |

$29,200 |

$31,500 |

$32,200 |

|

Married Filing Separately |

$14,600 |

$15,750 |

$16,100 |

|

Head of Household |

$21,9001 |

$23,6252 |

$24,1503 |

For tax year 2025 (and the returns you’ll file in early 2026), the standard deduction is $15,750 for single tax filers and those married filing separately, $31,500 for married filing jointly, and $23,625 for heads of household.4

A few things to keep in mind:

- If you’re either blind or over the age of 65, your standard deduction increases by $1,600 or $2,000 depending on your filing status. If you’re over 65 and blind, your deduction increases by another $1,600 or $2,000—again, depending on your filing status.5

- On top of that, the One Big Beautiful Bill Act (OBBBA) introduced a new (but temporary) extra $6,000 boost to the standard deduction for those age 65 and older. This tax break is available from 2025 to 2028.6

- You can’t use the standard deduction if you’re married filing separately and your spouse itemizes. That means you and your spouse need to get on the same page about which deduction will work best for you (and yes, you can use date night to talk about taxes if that’s the only way to get it done).

- If someone can claim you as a dependent, your standard deduction will be lower.

Now, if you choose the standard deduction, you don’t get to choose the amount deducted—what you see is what you get. But you also don’t have to mess with all the receipts and calculations that itemized deductions require. And what’s more, the standard deduction is a big enough number that most people don’t need to bother itemizing.

What Are Itemized Deductions?

Itemized deductions are certain amounts (the IRS calls them qualified expenses) you can subtract from your taxable income to lower your tax burden.

We’ll get into the nuts and bolts in a second, but not every expense qualifies as a deduction with the IRS. So yeah, that morning coffee run probably isn’t deductible (even if it is how business gets done).

Generally, taxpayers who itemize do so because it allows them to reduce their taxable income by even more than the standard deduction—which makes it worthwhile to track your expenses throughout the year.

But that’s the thing: Itemizing your deductions takes some work. Go ahead and save those expense receipts—but don’t just stuff them in a drawer or shoebox. When Tax Day comes around, you’ll be glad you kept organized files or made that spreadsheet (and updated it as needed).

When Should I Take the Standard Deduction?

It’s simple: Take the standard deduction when it’s larger than your itemized deductions.

You’ll want to know what expenses qualify as deductions in your situation, and there are plenty of rules to learn. But once you know the total of your itemized deductions, you can just compare it to the standard deduction and pick the bigger number.

Since Congress nearly doubled the standard deduction back in 2017, the vast majority of taxpayers (about 90%) choose the standard deduction’s set dollar amount over itemizing.7 And the good news is, the Tax Man increases the standard deduction every year to adjust for inflation. Hooray! Except the bad news is . . . the Tax Man. And inflation.

So, it might seem like a no-brainer to take the standard deduction, right? Less paperwork plus fewer hassles during the already-busy tax season equals “Yes, please!”

However . . . since this article covers both types of deductions, when exactly would someone choose to itemize? Let’s dig into that.

When Should I Itemize My Deductions?

This is a simple choice too: Itemize your deductions when they’re larger than the standard deduction.

When you maximize your deductions, you’ll see a difference in your tax bill. If you had a home mortgage (and you paid thousands in interest), plus you had to foot the bill for major out-of-pocket medical and dental expenses, your itemized deductions might add up to more than the standard deduction.

Here’s an example: Let’s say you’re married filing jointly, and you itemize $32,500 in deductions. That’s $1,000 more than the standard deduction for 2025, and that’s great. But it doesn’t mean you’ll save $1,000 in taxes (remember, deductions are subtracted from your taxable income). If you’re solidly in the 22% tax bracket, every dollar you deduct from your taxable income lowers your tax bill by 22 cents—which in this case is a tax savings of $220. Not too shabby!

See? It’s worth doing the math. Whenever those qualified expenses add up to more than the standard deduction, we’re itemizing, baby! Because if your number one wealth-building tool is your income, why wouldn’t you want more of it in your hands?

What Expenses Can Be Itemized?

Maybe you noticed we’ve used the phrase qualified expenses a couple of times (listen, we’re just the messenger here). So, what the heck does it mean? It just means they’re the kind of expenses that legally qualify with the IRS as deductions. Here’s a handy breakdown of the most common ones:

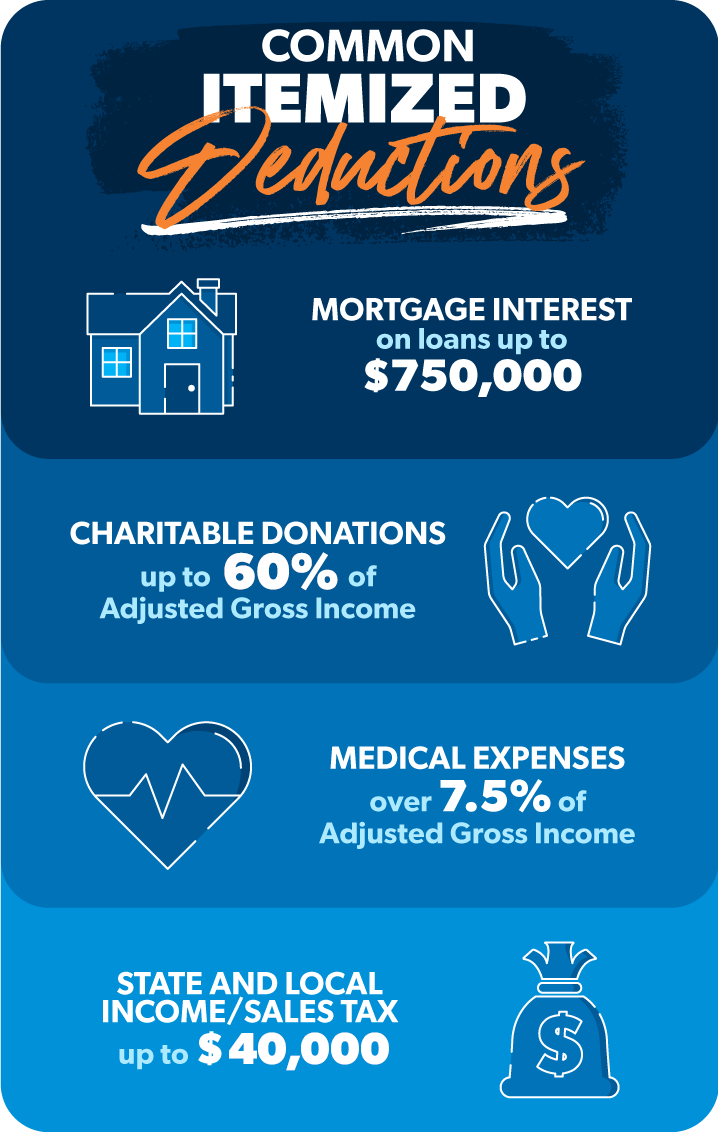

Mortgage Interest

The IRS allows you to deduct the interest you paid on your mortgage in a given tax year, but only for the first $750,000 (or $375,000 if married filing separately).

If you took out your home loan before December 16, 2017, you can deduct the interest for the first $1 million (or $500,000 if married filing separately).8

Charitable Donations

If you donated cash or property to nonprofits (like a community food bank, church or disaster relief fund), you can itemize those charitable donations up to an amount equal to 60% of your taxable income.9

If you do give cash, make sure to keep all receipts and paperwork. To deduct a cash donation of more than $250, you’ll need a receipt and a letter from the organization as documentation.10 As usual with taxes, planning and organization are key.

Medical Expenses

If you made more visits to your friendly neighborhood dentist this year than originally planned, we have good news (even if he’s unfriendly or not from your neighborhood). You can deduct any out-of-pocket medical or dental expenses that exceed 7.5% of your adjusted gross income (AGI).11

For example, if your AGI is $60,000, multiply that by 7.5% to see how high your out-of-pocket expenses have to be to qualify for this deduction (in this case, $4,500). So if you paid $5,025 out of pocket for a (way freaking expensive) root canal, you could add the difference, or $525, to your list of itemized deductions. Every little bit helps when you’re itemizing.

State and Local Taxes

The state and local tax (SALT) deduction allows you to deduct up to $40,000 ($20,000 if married filing separately) of your state and local property taxes, plus state income or sales taxes.12

Wait—did you catch that? Uncle Sam isn’t that generous. You can combine property and sales taxes or property and income taxes, but not all three.

Standard Deduction vs. Itemized Deductions: The Bottom Line

Let’s wrap it all up. For tax year 2025, here's when it makes sense to itemize your deductions.

- Single or married filing separately: Itemize your deductions if they add up to more than the standard deduction of $15,750.

- Married filing jointly: Itemize your deductions if they add up to more than the standard deduction of $31,500.

- Head of household: Itemize your deductions if they add up to more than the standard deduction of $23,625.

If you’re still on the fence about whether to itemize, go ahead and plug your numbers into your tax filing software—or check with a tax pro to see which option saves you the most money.

Other Tips to Get You Through Tax Season

Tax season comes around every year whether we like it or not. Tax Day, the big deadline to file your taxes, is usually April 15—and the sooner you start preparing, the better.

Tax time is stressful enough. If you’ve ever spent any amount of your valuable time digging through desk drawers and coat pockets searching for a missing expense receipt, you know the importance of staying organized.

So here’s a helpful tip: As you receive interest statements, 1099s, W-2s and other tax documents, file them together in a safe place (take photos and enter them in a spreadsheet) so they’ll be handy when you’re ready to start working on filing your taxes. Your future self will be like, “Thanks, me from a few months ago. That was super nice of you to be so organized.”

Next Steps

- Do you think it might make sense to itemize your deductions this year? Add up all your itemized deductions before deciding whether you’re going to take the standard deduction or itemize.

- If your tax situation has a few more moving parts, working with a tax pro is a smart move. RamseyTrusted® tax pros have years of experience and can help you file with confidence. Find your tax pro today!

- If your taxes are pretty simple and you want easy-to-use tax software that can give you a little more peace of mind, check out Ramsey SmartTax. No hidden fees, no ridiculous upcharges, no predatory loan offers. That’s how it should be!

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.