Key Takeaways

- A W-4 is an IRS document you fill out and give to your employer, usually on your first day at a new job, that tells your employer how much money to withhold from your paycheck to send to IRS for income taxes.

- Enter your personal information, then indicate if you have any additional jobs or if your spouse works.

- Claim your dependents and any other tax credits, then make any additional withholding adjustments.

- If you’ve had a major life-change, got a big tax refund, or got a big tax bill, you may want to revise your W-4.

Today’s the day! You woke up bright and early, strapped on your backpack, kissed your sweetheart goodbye, and headed off to your first day at a fancy new job. Woo-hoo!

Before you get cracking, there’s some stuff to get done—aka your onboarding paperwork. And one of the documents you’ll have to fill out is Form W-4. Yep—not the most exciting way to get started, but it’s an essential document when it comes to your taxes.

But don’t worry. A W-4 is really nothing to stress about. We’ll go over all the nitty-gritty details so you can fill out your W-4 with confidence, account for your tax credits and deductions, and keep the most money in your paycheck.

What Is Form W-4?

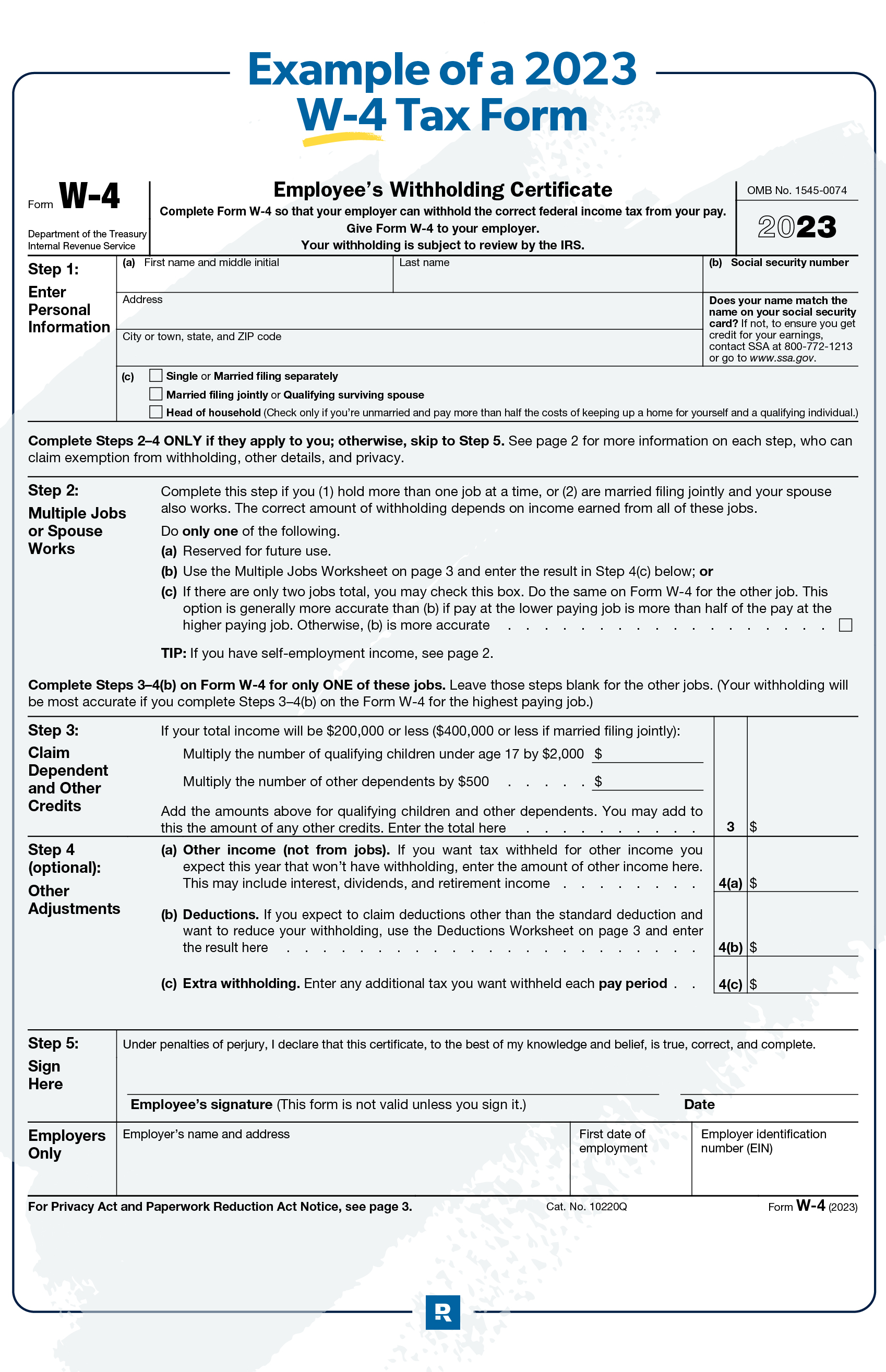

Form W-4 is an IRS document you fill out and give to your employer, usually on your first day at a new job. There are five steps, or sections, on Form W-4. Some of them might not apply to your current situation, which is why it’s important to know how every section affects your paycheck and income taxes.

What Is Form W-4 Used For?

Form W-4 tells your employer how much money to withhold from your paycheck to send to IRS for income taxes, which is called federal tax withholding. Yep. Uncle Sam wants his cut before you even see it.

The amount of money withheld depends on a few big things: how much money you make, your tax filing status, and how much you tell your employer to withhold on your W-4.

The money withheld counts toward your yearly income tax bill. You should fill out your W-4 so you owe the IRS nothing at tax time. On the flip side, having too much withheld from your paycheck means overpaying your taxes and results in a tax refund check. It’s basically the IRS returning money you’ve loaned them (interest-free, might we add) all year long.

Um . . . no thanks. Wouldn’t you much rather take home your hard-earned dollars on payday? Yeah, us too. Say it with us: “A refund is not a bonus!”

How to Fill Out a W-4 for a Job

Again, you’ll most likely fill out a W-4 on your first day at a new job as part of the employee onboarding process. If you work for a business from home, you’ll probably be asked to fill it out online.

Make sure you look over the form carefully, read all the directions, and confirm that you understand what each section means before moving on to the next. There’s no reason to rush.

And when in doubt, ask questions! Whoever’s onboarding you, whether it’s your new boss, a payroll manager or human resources rep, should be able to answer your questions and clear up any confusion.

How to Fill Out Your W-4: Step by Step

Like we said, there are five main sections, or steps, on the W-4, and not all of them may apply to your current situation. Here’s what to do:

Don’t settle for tax software with hidden fees or agendas. Use one that’s on your side—Ramsey SmartTax.

Step 1: Enter Personal Information

Fill out your name, address, and Social Security number. You’ll also add your anticipated tax filing status: single, married filing jointly, married filing separately, or head of household.

After this step, you have the option to skip right to Step 5, where you’ll sign your W-4 and have your employer withhold the standard amount for your salary and filing status.

But if you have dependents, multiple sources of income, or other deductions that raise or lower your tax liability (what you owe), you’ll have to dig into the next three steps to get your tax withholding just right. Otherwise, you’ll either overpay or underpay your taxes.

Step 2: Multiple Jobs or Spouse Works

In this section, you’ll indicate if you have a spouse who works (if married filing jointly) or if you have sources of income from other jobs or a side hustle.

This determines if your employer should withhold more or less from your paycheck than the standard withholding amount—what they’ll withhold if you just do Step 1 and Step 5 based on your income and filing status—so make sure you follow the directions listed out on the form.

For example, if you and your spouse make around the same amount of money, you’d both check box 2(c) based on the instructions on the form.1 If you have a larger pay gap between the two of you, the IRS provides worksheets to help you figure out the right amount of withholding.

And remember, if you have self-employment income from side work, there’s no employer to withhold taxes for you. But you still have to pay up.2

If you calculate what you’ll owe on that income and have those taxes withheld here on your W-4, you can avoid a surprise tax bill in April. And trust us, you really want to avoid that. (There are other ways of paying self-employment taxes, but this can be an easier option if you work an additional full- or part-time job.)

Step 3: Claim Dependent and Other Credits

Here’s where your kiddos and other dependents come in to help lower your taxes. Thanks to the child tax credit, if your total income is less than $200,000 ($400,000 for married filing jointly), you can claim $2,000 per child under the age of 17. And if you have other dependents, you can claim $500 each.3

Why claim dependent tax credits now instead of exclusively on your return? Well, if you do this now, you’ll keep that money in your paycheck instead of sending it off to Uncle Sam just so he can give it back to you later as a refund. Imagine all the diapers and school supplies you can buy throughout the year with that cash in your pocket.

You can also reflect any other credits you’re planning to claim on this step too. Just factor them into your total amount.

Step 4: Other Adjustments

Here's where you can note any other withholding adjustments, such as other sources of income not from jobs (like retirement investments), deductions you expect to claim, or extra money you’d like withheld.

Even though this step is listed as optional, it can be very important when it comes to getting your withholding right, especially when you’re adjusting your withholding after getting a tax bill.

Step 5: Sign Here

You made it! Now all you have to do is sign your John Hancock and boom—you’re all done.

How to Fill Out Your W-4 if You’re Married and You Both Work

When you and your spouse both have jobs, filling out your W-4 requires a little bit of communication and teamwork. So why not make your next date night a chat about your W-4s date night? Okay, you can come up with a better name, but you get the picture. We heard red wine pairs amazingly with financial wellness.

Download and print a sample Form W-4 from the IRS website so you can run through all the steps together.4 If you both work, you should each fill out your own version of the form and compare notes.

Keep this in mind: Only one of you should claim your dependent credits and deductions on the W-4. Otherwise, you’ll underpay your taxes.

This part can get tricky, especially if there are a lot of factors at play. So, make sure you coordinate with your spouse. And if you have a more complicated situation, it’s smart to connect with a tax pro. They’ll walk you through it all.

How to Fill Out Your W-4 if You’re a Student

Look, if you’re a younger student (and still a dependent), you probably won’t make enough money to have to file a tax return.5 When you start a new job and get a W-4, be sure to look it over, but don’t sweat it if you’re only filling out sections one and five since you probably don’t have dependents or deductions yet.

But if you work multiple jobs, you’ll want to complete Step 2. Even if you don’t make enough money to pay federal income taxes, you still have to pay into Social Security and Medicare (or FICA). This section makes sure those taxes are withheld so you don’t get a tax bill. Yep—even if you’re just mowing lawns on the weekends for extra cash. Any amount over $400 is subject to FICA taxes.6

How to Claim Allowances on Your W-4

You don’t. Well, not anymore at least. Back in 2020, the IRS revamped the W-4, dropping the number of sections from seven to five.7 Since there’s no longer a section for allowances (claiming a 1 or 0), you only use the current steps to figure out your paycheck withholding.

So, if you haven’t looked at your W-4 in several years and need to revise it (more on that below), make sure you understand the steps we walked through above.

Why You Might Want to Revise Your W-4

There are three main reasons to revise or adjust the tax withholding on your W-4:

1. You’ve had a major life-change.

Got some big lif- changes coming your way? Well, you might want to take another look at your W-4. Major life-changes that significantly alter your income or filing status can affect how much your employer should withhold for taxes. This includes life events like:

- You got married or divorced.

- You had or adopted a child.

- You welcomed an additional dependent into your household.

- You got a second job or started a side hustle.

- You were unemployed for part of the year.

2. You got a tax refund.

As we’ve mentioned, a tax refund is not a bonus. Some people see it as an extra chunk of change they can use to fund their next tropical getaway or big fancy purchase (like that seven-person deluxe Jacuzzi that conveniently had its price “slashed” in April). You’re not a kid on Christmas morning and Uncle Sam certainly isn’t jolly old St. Nick.

Adjust your W-4 accordingly and make sure you’re taking home the most money you can on payday without owing a tax bill. Seriously, think of all the things you could use that extra cash for right now. You could:

- Pay off debt faster.

- Quickly build an emergency fund.

- Save more for retirement.

- Make extra payments on your mortgage.

Keep your W-4 up to date with all those sweet credits and deductions and bring that bacon home on payday.

3. You got a tax bill.

There’s nothing more deflating than doing your tax return and getting blindsided by a chunky tax bill. While there’s not much you can do about it now except hunker down and get that bad boy paid off (you have options), you can avoid it next year.

Snag a copy of your W-4 and make sure your tax filing status is up to date and you’re taking all the credits and deductions you qualify for. You can also divide up your tax bill by your company’s pay periods (for example, if you get bimonthly paychecks, you’d have 24 pay periods), and the result will be the additional money you should withhold.

One of the easiest ways to make this adjustment is to add the result to your extra withholding on line 4(c) on Step 4.

How to Check and Change Your W-4

The good news is that with a little math and a bit of brainpower, you can easily adjust the tax withholding on your W-4. And remember, you can get a copy of and change your W-4 whenever you want and as many times as you want. So, there’s really no reason to put off important adjustments after a big life-change or a few not-so-awesome surprises during tax season.

Remember, zero is the magic number here—big goose egg! You only want to pay the IRS exactly what you owe them throughout the year. Nothing more, nothing less.

Do Taxes the Right Way

Okay, we get it. That’s a lot to get right on your W-4. But you don’t have to dig through the numbers alone. If you’ve got a complicated tax situation and you can’t get your W-4 just right on your own (think Goldilocks-style), reach out to a RamseyTrusted tax pro.

They’ll help make sense of your personal tax situation and guide you toward getting your W-4 right on the money (literally) so you can keep the most cash in your paycheck on payday.

Feeling confident about your W-4 and have a relatively simple return at tax time? Check out Ramsey SmartTax. It’s an affordable and easy-to-navigate tax software that helps you file your taxes with confidence. No hidden fees. Ever.

Frequently Asked Questions

-

Do I need to update my W-4 every year?

-

Nope. But you should update your W-4 whenever you’ve had a major life-change—like getting married, having kids, or starting a new job—or if you got a big tax refund or tax bill last tax season.

-

What’s the difference between a W-2 and a W-4?

-

Form W-4 is for telling your employer how much money to withhold from your paycheck to pay federal income taxes, called federal tax withholding. You complete the form and give it to your employer, usually on the first day at a new job. But you can also make adjustments whenever you want.

Form W-2 is given to you by your employer at the start of tax season, usually in January. This form summarizes your earnings—how much money you made—and how much you paid in taxes throughout the year. You use this form to fill out your annual tax return.

Did you find this article helpful? Share it!

About the author

Ramsey Solutions