Ramsey’s Complete Guide to Investing

Taking Your Investing to the Next Level

Imagine this. You don’t owe a single penny of consumer debt to anyone and you have a fully funded emergency fund in place. You’re climbing the corporate ladder or blazing a trail as an entrepreneur in the marketplace, and your income keeps rising with every promotion and sales milestone. You’re maxing out your retirement accounts and, shoot, maybe you’re even sitting in a paid-for house at this point.

In other words, you’re absolutely killing it. Way to go!

Once you’ve hit this point, you might be looking around for other ways to invest. Or, maybe your income is high enough that you’re maxing out your 401(k) and IRA options before you reach your 15% goal. If you’re in that boat, don’t worry—you have options. Let’s talk about them.

The Backdoor Roth IRA

It’s a frustrating fact of investing that there are income limits on who can invest in a Roth IRA. Once you hit a certain income, you can only contribute a limited amount, until you’re phased out completely.3 (There are no income limits on traditional IRAs, which will come in handy in a second.)

This is where a backdoor Roth IRA comes in.

A backdoor Roth IRA is an investment strategy that allows high-income earners to take advantage of tax-free investment growth and tax-free withdrawals in retirement. And don’t worry—it’s completely legit.

Here’s how this works: First you invest in a traditional IRA and then transfer or roll that money over into a Roth IRA. The only catch is that you’ll need to pay income taxes on the money you convert from the traditional IRA to the Roth IRA, and you’ll need to cover that with cash on hand. It’s a good idea to chat with your tax advisor, though, to get a clear picture of the tax implications before you make this move.

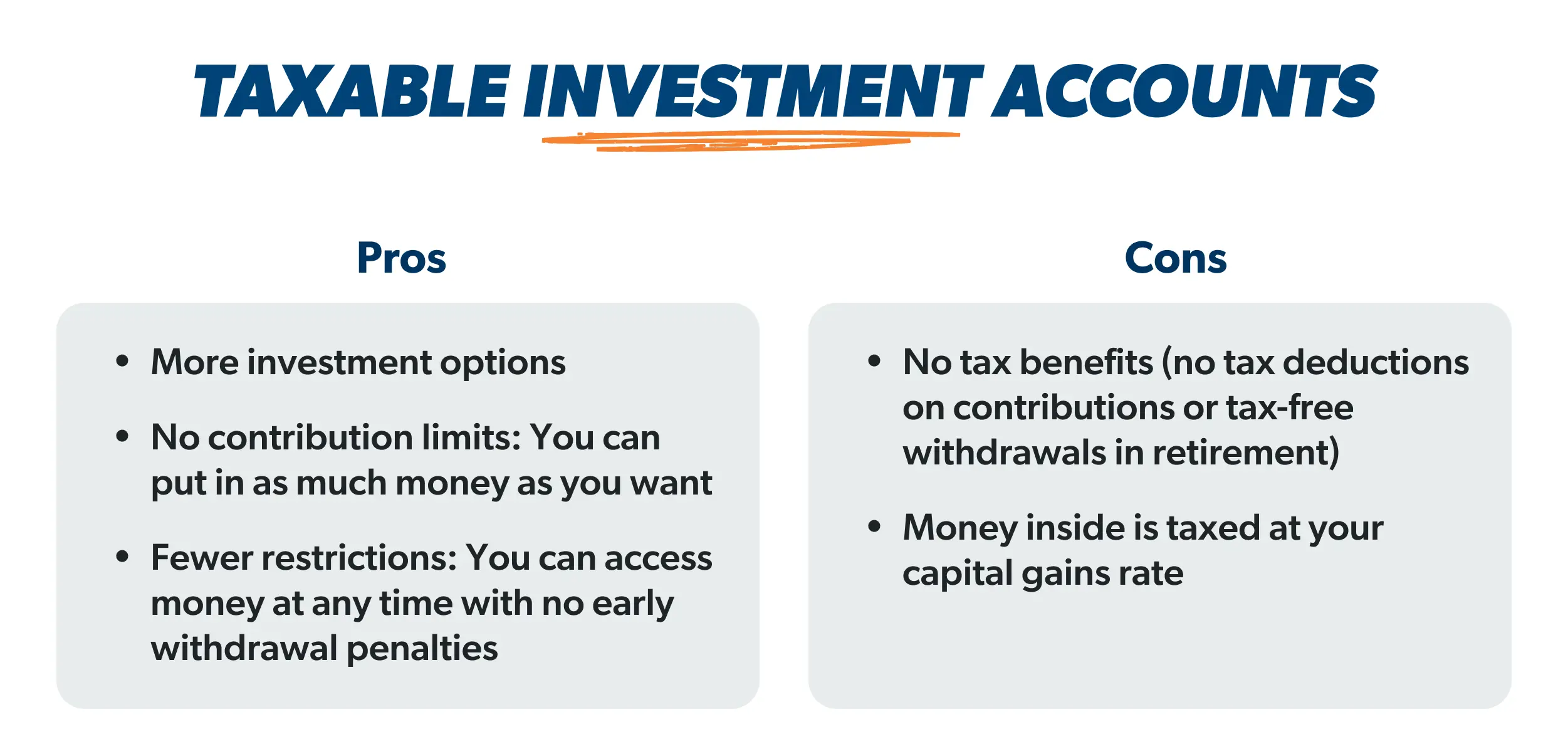

Taxable Investment Accounts

Taxable investment accounts (also known as brokerage accounts) let you invest in the same mutual funds you invest in through your tax-advantaged IRA . . . minus the tax advantages. Instead, your investments will be taxed at your capital gains tax rate. No tax-deferred contributions. No tax-free growth or tax-free withdrawals in retirement.

But the good news is that they don’t come with the contribution limits and rules that sometimes feel like a straitjacket for high-income earners who want to invest more than tax-advantaged retirement accounts allow.

For those of you dreaming about an early retirement, taxable investment accounts are the perfect way to create a “bridge account” that will help you bridge the gap (get it?) between when you want to retire and when you can start taking money out of your tax-advantaged retirement accounts without penalties (age 59 1/2).

Health Savings Accounts (HSAs)

Health savings accounts are tax-advantaged savings accounts that can help you pay for medical expenses tax-free now and in the future. It’s like an extra emergency fund just for medical costs!

HSAs come with a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Plus, you own your HSA (which means it goes with you even if you change jobs) and your account balance rolls over each year.

Just keep in mind that if you want to open and put money into an HSA, you must also have a high-deductible health plan (HDHP). These health insurance plans generally have lower premiums, but you’ll cover more of your health care costs yourself before the insurance company starts to kick in.

We know what you’re thinking: What does a savings account designed to pay for medical expenses have to do with investing? Well, one of the things we love most about HSAs is that you can invest your HSA money in mutual funds once your account balance hits a certain threshold (usually $1,000) so that the money you put into it can grow over the long term. Plus, that HSA will act like a traditional IRA once you turn 65 years old (and you can still pay medical expenses from your HSA tax-free)!

That’s why we like to call it the “Health IRA,” because if you don’t use your HSA very often it can be another easy way to save and invest for retirement with some great tax perks.

Investing in Real Estate

And then there’s everyone’s favorite investment opportunity—real estate! You can make money from real estate in three ways:

- Increase in property value: When the value of your properties increases over time, you can make a profit when you sell those properties (this is also called appreciated value). A property’s value can rise fairly quickly, like it does with house flippers who buy properties, fix them up, and then sell them for a higher price than they bought them for. Or it can happen naturally as the value of your investment property increases as home values rise in your area. (Side note: Don’t forget about taxes! Any profit you make from the sale of a rental property is subject to capital gains taxes and rental income is taxed at your standard income tax rates.)

- Cash flow: This comes in the form of rental income, the money you regularly receive from folks who rent property you own.

- Depreciation: If you feel like you paid a small fortune to buy a rental property, we have some good news. You can write off a portion of the cost of the property each year from your taxable income by factoring in the assumed drop in the property’s value over time. This deduction will likely offset the taxes you owe on your rental income, making most of it tax-free (or close to it). This is next-level tax stuff, so you should talk with your tax advisor about tax breaks for your rental properties.

Now listen, before you go out and decide to become a real estate mogul because you watched one too many HGTV shows last weekend, here are some ground rules for investing in real estate.

1. Pay cash for real estate investments.

First, you should only buy a rental property if you have a fully funded emergency fund in place and you can pay for the property in full with cash. You read that right—if you can’t pay cash for the property, you’re not ready to invest in real estate. No exceptions! Taking out a mortgage for your home is one thing, but going into debt for an investment property will add more risk to your financial life than you need.

This is why we recommend you pay off the mortgage on your personal home before you make plans to invest in real estate. With no more mortgage payments to worry about, you’ll have a lot more money to put toward other investments, like your 401(k), real estate, and Taylor Swift tickets (we’re kidding about that last one, kind of).

2. Start small and stay local.

If you’re just getting into the real estate business, maybe don’t start with a mansion. This isn’t about going big or going home. Find a condo or townhome in an affordable neighborhood and start there.

And remember that old saying: Keep your friends close, and your investment properties closer. Okay, that’s not how the saying goes—but it still works. You want to be close enough to your properties to keep an eye on your investments and address any problems that might pop up. If you live in Georgia, for example, don’t buy a property in Minnesota!

3. Work with a real estate agent.

And finally, don’t try to find properties on your own. Work with a real estate agent who knows the area well and can help you spot properties that will give you the best return on your investment.