Ramsey’s Complete Guide to Investing

How to Pick Your Investments

Trying to pick the right investments can feel pretty daunting and intimidating . . . like when you’re at the grocery store trying to find the avocado that’ll be just ripe enough for the avocado toast you want to make at home the next morning (Pro tip: Look for the darker avocados that give slightly when you apply firm, gentle, pressure. You’re welcome!).

Deciding what to put into your investment portfolio is a big deal. But when you know what to look for, choosing the right investments will feel a lot less complicated!

1. Mutual funds are the way to go.

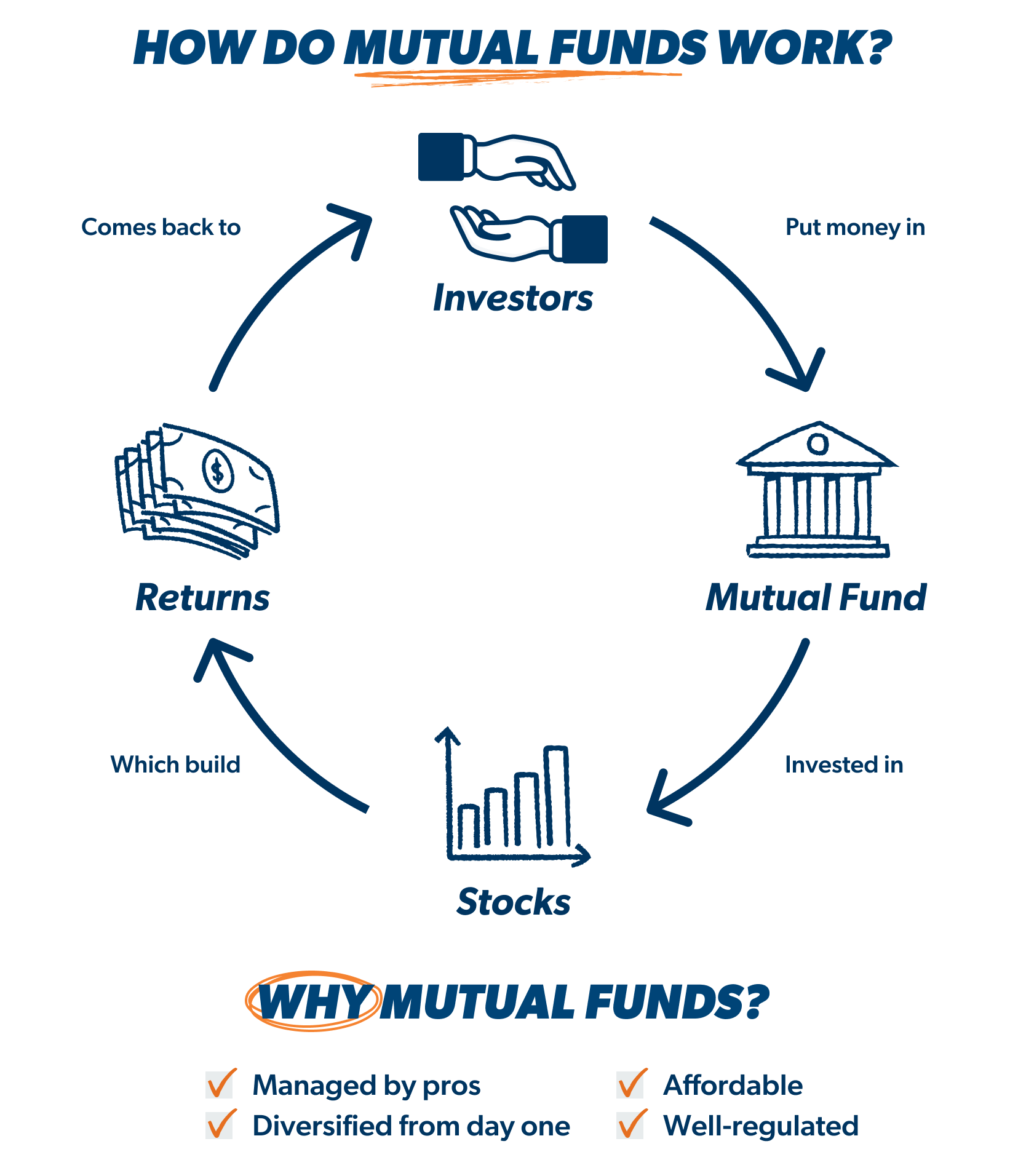

Let’s talk about mutual funds. Mutual funds are investments that allow investors to pool their money together to invest in something—like stocks, bonds or other investment options.

Stock mutual funds are our choice for retirement investing because they let you invest in shares of stock from dozens or even hundreds of companies at once. That helps you diversify your investments, which is another way of saying you’re not putting all your eggs in one basket like you would if you invested in single stocks. Single stocks are way too risky to build your retirement future on.

Mutual funds are managed by a team of investment pros, and their job is to choose stocks for the fund that will consistently outperform the stock market or a certain index, like the S&P 500, which makes them great options for long-term investors saving for retirement.

2. Diversify your portfolio with different types of mutual funds.

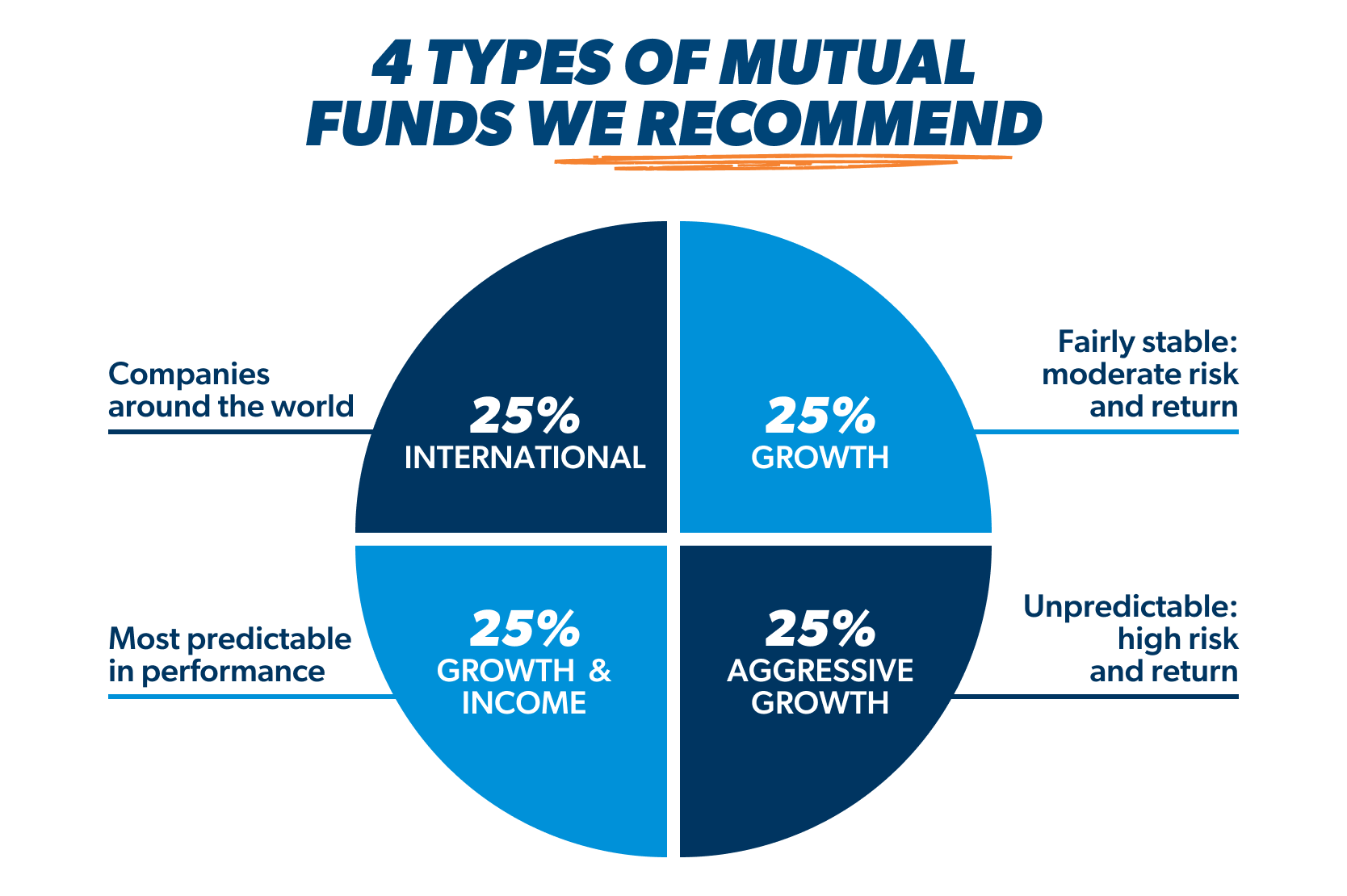

We recommend going a step further and spreading your investments equally between four different types of growth stock mutual funds: growth and income, growth, aggressive growth, and international.

Putting 25% of your investment money into each of these four types of funds helps you take advantage of the stock market’s growth over time while lowering your investment risk because you’ll be investing in different sectors of the stock market and different parts of the world.

Let’s break each of those mutual funds down real quick so you know exactly what you’re investing in.

Growth and Income Funds (Large-Cap)

Sometimes known as large-cap growth funds, growth and income funds will usually be the calmest, most stable funds in your portfolio. Their goal is to give investors slow and steady growth by investing in large, established companies that experience fewer ups and downs than smaller companies. These funds usually contain a blend of growth and value stocks (we talked about those in the last chapter) to provide a stable foundation for your portfolio.

Growth Funds (Mid-Cap)

Growth (or mid-cap) funds invest in medium-sized company stocks, which offer better potential for higher returns than large-cap funds while carrying less risk than small-cap funds, which invest in smaller, newer, “high-risk, high-reward” companies. Speaking of which . . .

Aggressive Growth Funds (Small-Cap)

Also called emerging market funds or small-cap funds, this fund will be the “wild child” of your portfolio. These funds often invest in startups that could potentially become the next big thing . . . or complete busts. It’s really important to balance these funds with the less volatile mutual funds we just talked about!

International Funds

Made up of companies from around the world, international funds help you diversify your portfolio even more by investing in often well-known companies based outside of the United States.

3. Pick mutual funds with a long track record of success.

When you pick mutual funds, remember to look for funds that have a track record of strong returns over a long period of time. That means the fund should at least be 10 years old and have consistently outperformed the fund’s category index over time.

An easy way to check this is to take a look at a fund’s prospectus before you decide to invest in it. A prospectus is a document that has all the details you need to know about a particular mutual fund, including its investment objectives, historic performance, fee structure and fund management.

4. Pay attention to investment fees.

While you can’t completely escape the fees that come with investing, excessive investment fees can cut into the growth of your investments if you’re not careful.

It’s important to keep an eye on the following types of investment fees before you buy a mutual fund:

- Loads (sales commissions): The investment pro you’re buying mutual funds from will usually get a small percentage of the money you invest, otherwise known as a load.

- Expense ratios (annual fund operating expenses): This fee helps cover the costs of running the mutual fund and will be a percentage of your investment account balance.

- Advisor fees: If your pro charges an advisor fee as part of their payment structure, it might show up as an assets-under-management fee. This usually means your pro is charging you a percentage of how much money they manage for you each year.

When you work with a pro to buy mutual funds, always ask how they’re paid and how those fees might impact the growth of your investments. But don’t get so caught up with trying to find the cheapest fees that you miss out on a good investment or help from an advisor you trust. Look for funds with a reasonable expense ratio with a long-term track record of excellent returns and good management in place. That’s a winning combination!