Ramsey’s Complete Guide to Investing

Most Common Investing Mistakes to Avoid

Listen, we all make mistakes. Who among us hasn’t accidentally hit “Reply All” on a company-wide email or forgotten to wish an important someone a happy birthday? Sorry, Mom . . .

But some of the worst mistakes you can make come with investing: The missteps you make today could lead to regret and panic when you get close to retirement age.

And listen, maybe you’ve made one of the mistakes below. That’s okay. All of us have done dumb things with money. But we want you to hear us loud and clear—there is always time to get back on track. So don’t give up! We’ll show you how you can pick yourself up and get back in the race.

Mistake 1: Not Saving Enough for Retirement

We mentioned before that research shows over and over again that the top indicator of investment success is your savings rate.4 Your savings rate is how much you save and how often you do it. Figuring out rates of return, asset allocation and expense ratios is all fine and dandy, but they won’t mean a thing if you never actually put any money in your 401(k)!

We have found that investing 15% of your income consistently over time, no matter what your income is, will put you in a strong position to retire with a nice, big nest egg. And you’ll still have enough margin to save up for other important financial goals at the same time—like saving up for your kids’ college funds and paying off your house early.

If you’re curious about how much you can have saved up for retirement by investing 15% of your income, you can check out our investment calculator to see how investing different amounts of your income will impact the size of your nest egg over time.

Mistake 2: Treating Your 401(k) Like an Emergency Fund

Cracking into your 401(k) early and often is a huge mistake that could cost you hundreds of thousands of dollars over the long run. For starters, there’s the 10% early withdrawal penalty for taking money out of your account before age 59 1/2. And then there’s the income tax hit on traditional 401(k) withdrawals and the pre-tax portion of your Roth 401(k) only.

So, if you’re in the 22% tax bracket, that means a $10,000 withdrawal becomes just $6,800 with one snap of Uncle Sam’s fingers after taxes and penalties (and we didn’t even talk about state income taxes). Ouch.

But the real pain comes when you crunch the numbers on how much that early withdrawal will cost you in the long run. If you take out $10,000 from your 401(k) that was invested in good growth stock mutual funds at age 35, that withdrawal could leave you with $267,000 less in your nest egg when you retire at age 65. Let that sink in for a minute.

This is why you need that fully funded emergency fund in place (that’s 3–6 months’ worth of expenses saved up) before you invest a single penny. You’ll thank yourself later!

Mistake 3: Investing While You’re Still in Debt

Your income is your most important wealth-building tool. And as long you’re still in debt and paying hundreds (or even thousands) of dollars on loans, credit cards and other forms of debt, you’re never going to see the progress you want to make with your investments. Investing with debt is like trying to chop down a tree with a dull axe—either you’re going to get tired and give up, or you’re going to hurt yourself in the process.

If you’re the average American carrying around a car loan, credit cards and a student loan, that means you’re probably paying about $1,270 toward your debts every . . . single . . . month.5

Freeing up that money and investing it instead could make you a millionaire in 20 years or less. That should light a fire under you to get those debts out of your life so you can unlock your full wealth-building potential!

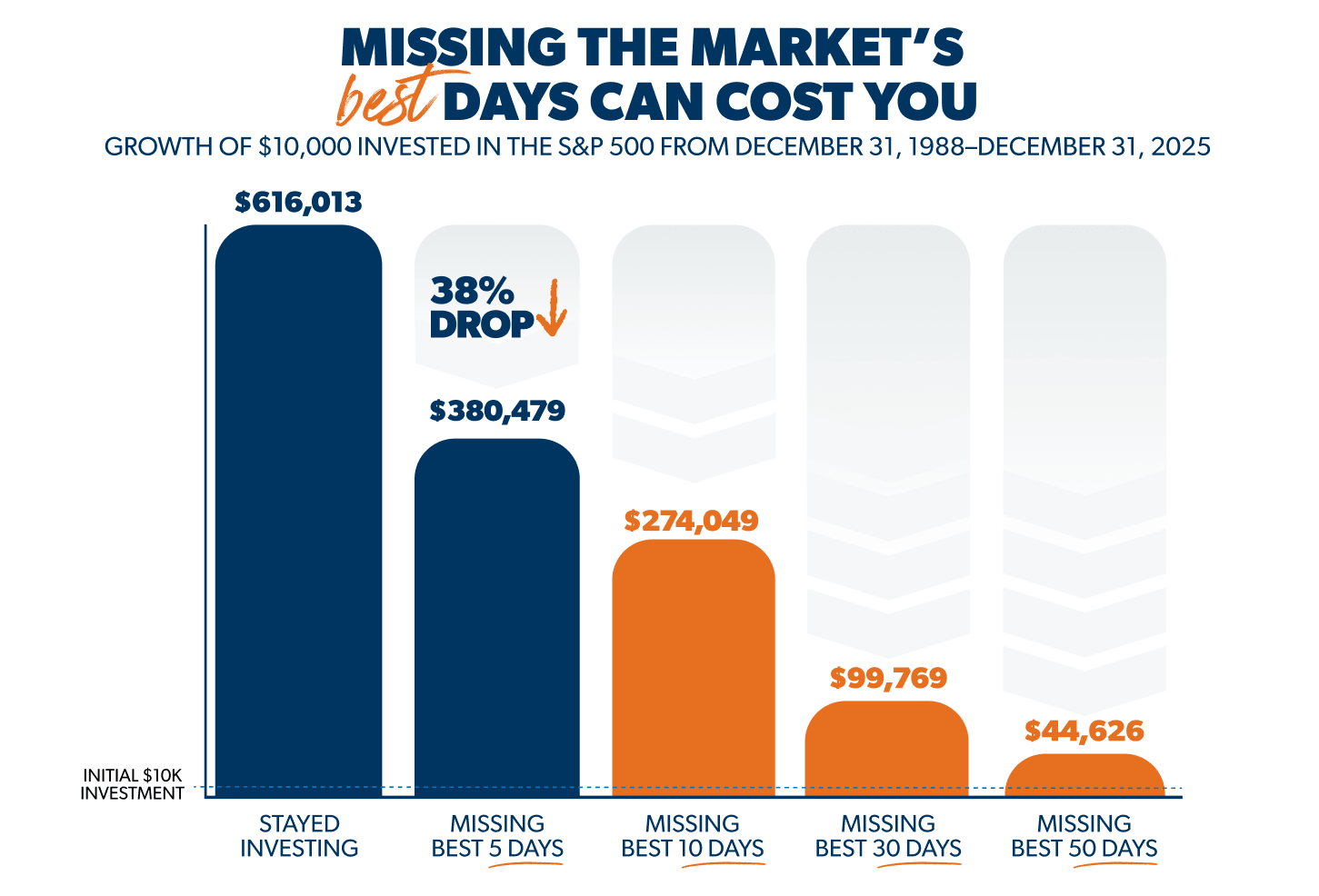

Mistake 4: Panicking When There’s a Market Downturn

The stock market is like a roller coaster—and the last thing you want to do is jump off in the middle of the ride. Too many people pull their money out of their investments and retirement accounts when the market is at its lowest—which is the worst possible time to do that.

You see, whether we’re in the middle of a stock market rally or a years-long recession, as long as your money stays invested in your 401(k) or IRA, you haven’t lost or gained anything. There’s a fancy term for that—unrealized losses or unrealized gains. That just means it’s all on paper. But the moment you take your money out, that’s when you’ve locked in your losses.

That’s why it’s so important to keep a cool head and a long-term perspective when it comes to investing. The stock market, for all its ups and downs, has always trended upward and rewards investors’ patience through the good times and the bad!

If you’re struggling with the emotional ups and downs of the stock market, that’s normal. When that happens, it might help to talk things through with a financial advisor who can truly help you figure out whether or not you need to make any changes or just sit tight.