Ramsey’s Complete Guide to Investing

Before You Start Investing: Setting a Foundation

Ask any homebuilder what the most important part of a house is and they’ll likely tell you the same thing—it’s all about the foundation. You can build the most beautiful home in the world but if you build it on top of a shaky foundation, you’ll soon have cracks in the walls and wonky floors. The whole thing could come crashing down at any moment.

The same can happen with your retirement savings if you don’t have the right financial foundation in place. That’s why there are some things you must do before you start investing your hard-earned money.

1. Get rid of all your consumer debt.

Your income is your most powerful wealth-building tool. When your income is freed up to save and invest, you can put it to work to build wealth and reach your financial goals. But when you send hundreds of dollars out to make credit card, student loan and car payments every month, that completely robs you of your wealth-building potential. That’s normal in America—and normal is broke.

If you still have consumer debt, stop any investing you’re doing and get out of debt using the debt snowball. List your debts from smallest to largest (regardless of interest rate). Pay the minimum payment on all of them except the smallest one, and attack that one with a vengeance until you pay it off. Then roll what you were paying on that debt into the payment on the next smallest debt. Keep the snowball rolling until all your debt is paid off.

When you can finally scream that you are debt-free, you’ve set the cornerstone for a financial foundation that will allow you to invest with confidence and experience a freedom you’ve never had before.

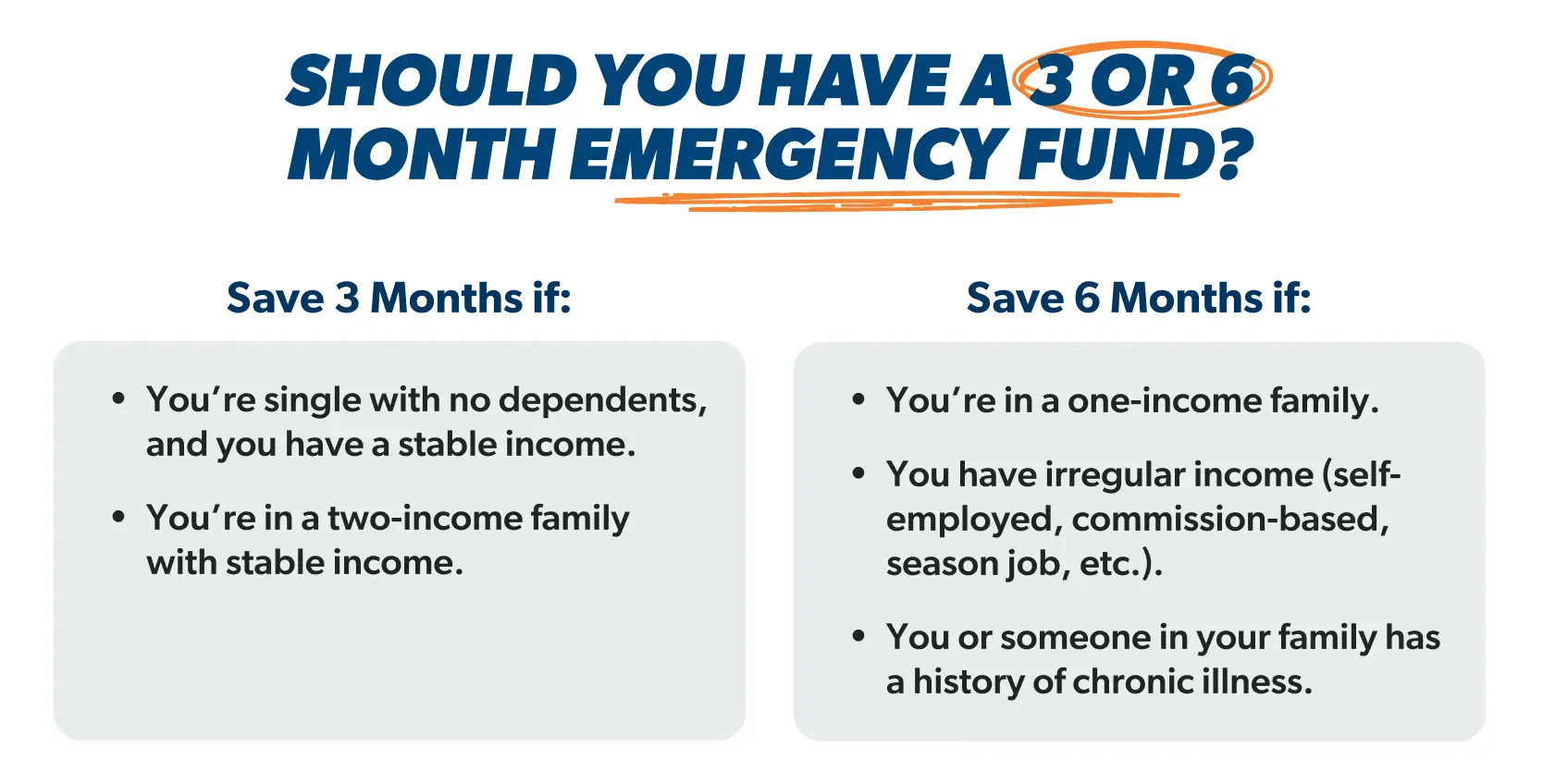

2. Have a fully funded emergency fund in place.

Once you’re out of debt, finish up that foundation by building up an emergency fund with 3–6 months’ worth of expenses saved in a high-yield savings account or money market account. When you do that before you start investing, you’ll have enough cash on hand (that’s also in an easily accessible place) to keep most emergencies from derailing your financial plan.

When you don’t have emergency savings in place, your 401(k) suddenly starts to look more like a piggy bank instead of a retirement account. You’ll end up like a lot of folks these days who treat their 401(k) like an ATM when they’re in a crunch and need some quick cash.1

Let’s be clear: Taking money out of your 401(k) early is a huge mistake. When you withdraw money from your 401(k) before age 59 1/2, you’ll pay early withdrawal penalties and taxes on the money you take out. But that’s not the worst part. The worst part is that you’re undercutting your own nest egg and potentially missing out on hundreds of thousands of dollars in investment growth over time.

3. Set a retirement savings goal.

A dream without a goal is just a wish. Whether you want to make more friends, get ahead in your career, or get in shape, goals help you get to where you want to go and become the person you want to be. They help you get from point A to point B. And retirement planning is no different—you need a goal to aim at so you can stay on track.

Take some time to sit down with your spouse or a good friend and think about what kind of retirement you want. Do you want to travel around the world? Spend lots of time with your grandkids? Become a pickleball pro? The more specific you can get, the better!

Then, you can use our free retirement assessment tool to figure out how much money you’ll need in your nest egg for the lifestyle you want, and how much you’ll need to invest every month to help you get there.

You might need to revisit and adjust your retirement savings goals from time to time, but having a target to aim at and a high-definition retirement dream in mind will help keep you motivated for the long haul!