Link copied!

Unable to copy link. Please try again.

If you’re wondering who is eligible for Medicare, then we’re willing to bet you haven’t yet been blessed with the monsoon of mailers screaming for you to pick them for your Medicare needs. Don’t worry. It’s coming—as soon as you get close to the big 6-5.

Meanwhile, we’ll do our best to answer the question Who is eligible for Medicare?

Medicare is the government’s answer to skyrocketing health insurance costs as folks age. It’s basically a federally run health insurance program for people over 65 and the disabled.

Key Takeaways

- To be eligible for Medicare, you must be age 65 or older, or be disabled, have end-stage renal disease, or have ALS (Lou Gehrig’s disease).

- Medicare is available for U.S. citizens or folks with legal residency.

- To be eligible for Medicare Part A premium-free, you must have worked and contributed to Social Security for at least 10 years.

Basic Eligibility Criteria

While there are a few different criteria of eligibility for different aspects within Medicare, the main criterion is your age.

Age Requirement

Basic eligibility for Medicare is pretty simple: You must be at least 65 years old.

Get help figuring out the Medicare plan that’s right for you. Talk to a licensed advisor for free.

Check out our chart with birth years to see when you’ll be eligible.

|

Medicare Eligibility Age Chart |

|

|

Birth Year |

Medicare eligible |

|

1959 |

2024 |

|

1960 |

2025 |

|

1961 |

2026 |

|

1962 |

2027 |

|

1963 |

2028 |

|

1964 |

2029 |

Citizenship and Residency Requirements

It may come as a surprise, but you need to be a U.S. citizen or at least have legal residency in the U.S. to be eligible for Medicare. Lawful permanent residents (LPRs) need to have lived in the U.S. for at least five years in a row before applying for Medicare.

Illegal immigrants aren’t eligible to get Medicare.

Eligibility Based on Work History

Medicare is funded by all the millions of people who work and pay the Social Security tax out of their paychecks. It wouldn’t be very fair if people who hadn’t worked a day in their lives could just sign up and get all the benefits of Medicare, so to get certain things like free premiums, the government added a work history qualification.

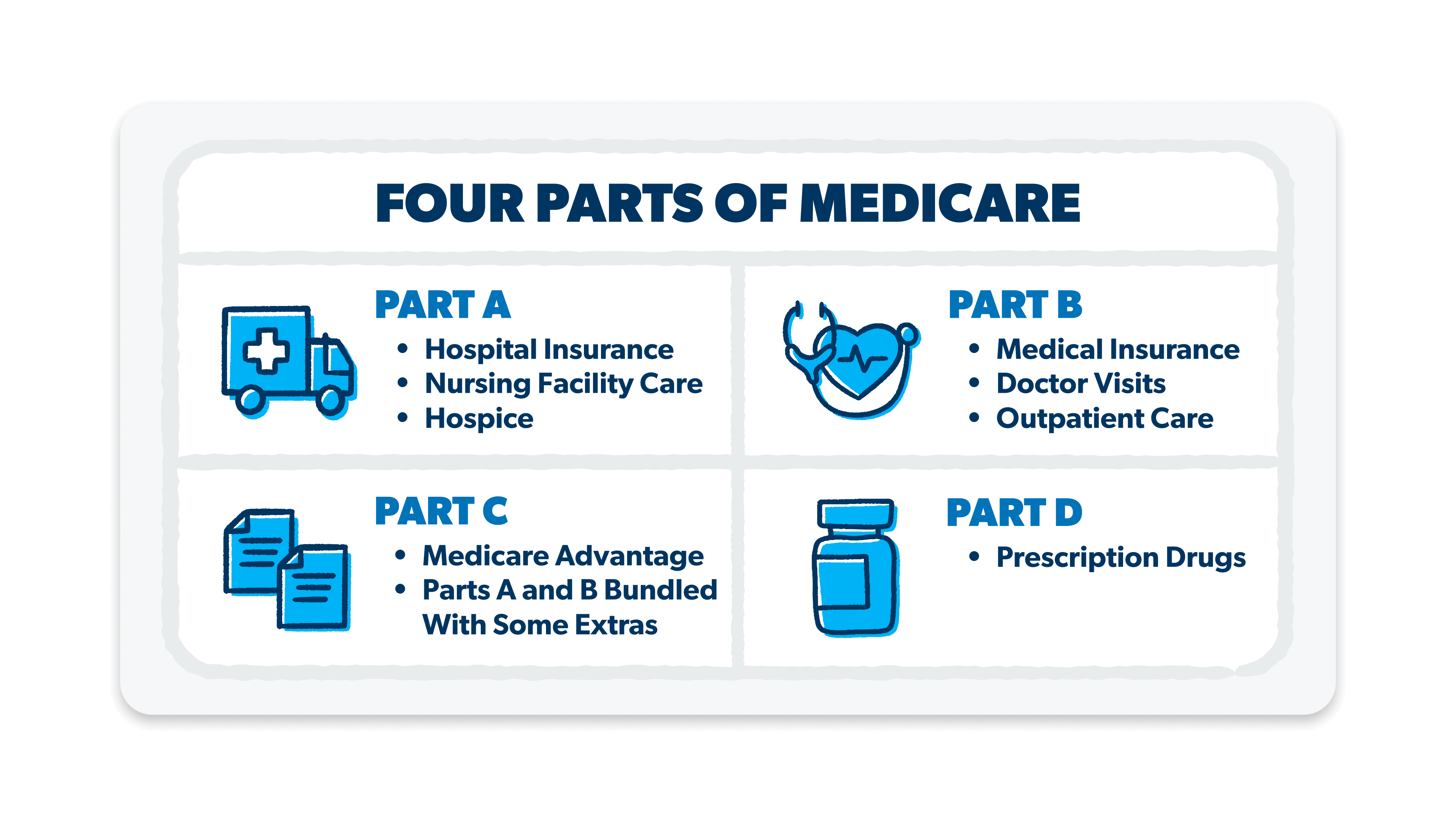

Eligibility for Medicare Part A (Hospital Insurance)

Generally, you have to have worked a job and paid the Social Security tax for at least 10 years (or 40 calendar quarters if you want to say it the confusing way) to qualify for premium-free Part A. Now, if you have a disability, everything changes. That’s when you qualify based on your health rather than your age and work history.

You may be thinking, Wait, I’ve been a stay-at-home-parent my whole working life—can I not get premium-free Part A? You probably can! You can qualify off your spouse’s work history—even if they’ve passed away or you’re divorced.

There are conditions though:

- You have to have been married for at least a year before applying.

- If you’re divorced, you have to have been married for at least 10 years and divorced for two.

- If your spouse has died, you have to have been married for at least nine months before they passed away, and you have to be single now.

Things get a little funky if you don’t qualify on your work history. Even if you can’t get free premiums with Part A, you can still buy Part A by paying premiums. But if you’re in this boat, you’re now also required to get Part B—it’s no longer optional. How high your premiums are for Part A will depend on how many yearly quarters you have been paying into Social Security. Part B premiums will be the same as everybody else.

There’s a chance you could be eligible to reduce or get rid of your Part A premiums in time if you keep working and paying into Social Security.

Here's A Tip

Here’s a Tip: If you haven’t worked and paid into Social Security the required 10 years to get a free premium with Part A, you’ll have to pay for Part A. But you can get your premiums reduced or knocked out altogether over time if you keep working.

Eligibility for Medicare Part B (Medical Insurance)

Since there are no free premiums offered with Part B, work history doesn’t come into play. As long as you meet the other requirements like being 65 years old, you’re eligible for Part B.

Medicare Tips That Set You Up for Success

Government programs are the best . . . at being confusing. And Medicare is no exception. But you can download a guide that makes learning the basics of Medicare feel like talking to a no-nonsense friend over coffee.

Eligibility for Medicare Part C (Medicare Advantage)

Reminder: Medicare Part C is actually a private Medicare plan that combines Parts A and B coverage with some private coverages and often includes Part D coverage as well. (If you want more info on the different kinds of Medicare, check out our article What Is Medicare and How Does It Work?)

To be eligible to sign up for a Medicare Advantage Plan, you must:

- Be enrolled in Medicare Parts A and B. (The same work history conditions apply when getting Medicare Part A premium-free.)

- Live in the area serviced by the plan you want.

- Be a U.S. citizen or LPR.

You can enroll for a Medicare Advantage plan, switch to a different one if you already have an Advantage plan, or drop it and go back to Original Medicare during the open enrollment period (January 1–March 31). Plan options vary by insurance company, so shop around.

Eligibility for Medicare Part D (Prescription Drug Coverage)

To get Part D, you have to be enrolled in either (or both) Part A or B. You can get Part D during your initial enrollment period or during the Medicare Advantage open enrollment period if you’re dropping a Medicare Advantage Plan and switching back to Original Medicare.

If you’ve got Medicare Advantage, you may already have prescription drug coverage included in your plan, so check to see if you even need to get Part D. If you don’t have drug coverage through another plan, it’s best to go ahead and sign up for Part D as soon as you’re eligible for Medicare. If it turns out you need it later, you’ll be penalized for signing up late.

Special Eligibility Situation

We mentioned earlier that there are situations where you become eligible for Medicare outside of turning 65. These situations are definitely not ideal, but if you find yourself in one of them, Medicare could be very helpful.

Individuals Under 65 With Disabilities

Below are the special cases where you can qualify at a younger age.

If you have been on disability for 24 months, you can get Medicare in your 25th month.

People with end-stage renal disease (you need dialysis or a kidney transplant) qualify to receive Medicare immediately. To get Part A with a free premium, you will still need to meet the work history requirement.

You would also qualify if you have been diagnosed with amyotrophic lateral sclerosis or ALS (aka Lou Gehrig’s disease). You are eligible as soon as you start receiving disability benefits (no 24-month waiting period) because ALS progresses so rapidly.

Enrollment Process

Once you know you’re eligible, it’s time to enroll! In fact, if you don’t enroll when you’re eligible, you could end up facing some penalties. (We’ll get to those in a minute.)

Initial Enrollment Period

Your initial enrollment period (IEP) is when you should sign up for Medicare if you don’t have any alternative coverage (like health care through your employer). We’re all for declaring a birthday month, but the government wants to celebrate for seven! Your IEP starts three months before your birthday month and goes through three months after your birthday month (keep the party going!).

When Will My Medicare Coverage Start?

|

When Will My Medicare Coverage Start? |

|

|

If you enroll: |

Your coverage starts: |

|

1–3 months before your 65th birthday |

In your birthday month |

|

In your birthday month |

The following month |

|

Within 3 months after your birthday month |

The following month |

If you still have coverage through work or the open marketplace, then you can wait to sign up for Part B. But you probably still want to sign up for Part A—because it’s free!

If you don’t sign up during your IEP and you don’t have comparable coverage, you will be penalized with higher monthly premiums for the rest of your life . . . Mwahahaha. We’re actually not joking. The government is really serious about people signing up for Medicare on time. In fact, the longer you wait, the higher your penalty will be.

Special Enrollment Periods

Sometimes you can qualify for a special enrollment period (SEP) if you have the right extenuating circumstances. Most of these only apply to people who:

- Already have a Medicare Advantage plan or

- Are signing up later for Medicare parts A, B, C and D because of having other health insurance coverage

The most common reason you’ll get a SEP with Medicare Advantage is if you move and your plan isn’t available in the area you moved to. In this case, you’ll get a window to change plans.

You can also qualify for a SEP if you turned 65 while living abroad. You’ll get a four-month SEP starting the month you return to U.S. soil.

You won’t be penalized if you use a SEP, but watch out—if you miss your SEP, you will probably have to pay a penalty when you do sign up.

General Enrollment Period

Speaking of late enrollment, the general enrollment period (GEP) is your second chance to sign up if you miss your IEP or SEP. If you have to use the GEP, you may get a penalty though. The GEP runs from January 1–March 31.

Find Help as You Shop Medicare

At this point, we’re stating the obvious, but—Medicare is complex. Just keeping the different enrollment periods straight is enough to make your brain melt. That’s why we encourage everyone to work with one of the RamseyTrusted advisors at Chapter Medicare.

They know the ins and outs of how Medicare works, which plans work better in what situations, and who’s eligible for what. Oh, and they’ll keep you straight on the enrollment periods too—so you don’t get penalized! An advisor from Chapter will listen to your situation and then shop from 24,000 plans to find you the perfect fit. After you’ve got your plan, they’ll keep checking in to make sure it’s working for you and answer any questions you have.

And did we mention it’s free? So talk with a Medicare advisor from Chapter. They’ll keep you from pulling your hair out over Medicare (and let’s face it, at this point, you need every hair you’ve got).

Next Steps

- Learn more about how Medicare works.

- Still not convinced you need an advisor? Check out all the ways they can help you (including saving you money)!

- Get in touch with Chapter to get advice just for you.

-

What if you are not eligible for premium-free Part A?

-

You can still buy Medicare Part A by paying monthly premiums. If you continue to work and pay into Social Security, you may eventually be able to reduce or eliminate your premiums for Part A.

-

How does Medicare interact with other insurance plans?

-

If you have regular health insurance through your employer or the open marketplace, that insurance pays first—so if you have Medicare, you often won’t pay anything.

-

What are the implications of moving or changing residency?

-

If you have Original Medicare and move to a different state, nothing will happen to your coverage because Medicare is run by the federal government and is standard across all states.

If you have Medicare Advantage, your plan may not be available in your new location. Medicare Advantage is run by private insurance companies with different networks in different areas. So if you move to an area where your current plan is unavailable, you may need to find a new Medicare Advantage Plan. If that happens, you’ll get a special enrollment period to find and enroll in a new plan.

Get Weekly Insights Delivered Straight to Your Inbox

Did you find this article helpful? Share it!

About the author

Ramsey Solutions

Get proven Ramsey answers fast.