How Much Does Long-Term Care Insurance Cost?

16 Min Read | Dec 18, 2024

What if I asked you, “Do you want to get older?” I’m pretty sure the answer would be, “Um, no thank you!” And I get it. Walkers and old-lady fashion are not my jam either. But old age is coming whether you want it to or not, and wouldn’t it be so much nicer to know you’re ready?

The truth is that long-term care (also called LTC) is expensive and getting expensiver (is that a word?). You need to have a plan to pay for it so you don’t get wrecked financially. That’s where long-term care insurance comes in.

Key Takeaways

- Long-term care costs are going up, so it’s important to buy long-term care insurance to protect your nest egg.

- Long-term care insurance costs are different for men and women. In 2023, the average 60-year-old man paid $1,200 per year for a level benefit policy that covered $165,000 in care. The average 60-year-old woman paid $1,960 for the same coverage.1

- You should wait to sign up for long-term care insurance until you’re 60.

What Is Long-Term Care Insurance?

Long-term care insurance is a policy that covers costs related to nursing home care, assisted living facilities, or caretakers coming to your house. It pays for support for those who can no longer perform everyday activities as they age.

It also covers things like home modifications, in-home caretakers, medical equipment and care coordination (or care management). Care coordination is a service that handles all aspects of long-term care, even finding it and managing schedules. All of this means you’ll potentially be able to live longer in the comfort of your own home. And who doesn’t want that, right?

Traditional long-term care insurance policies are triggered when you can no longer perform 2 out of 6 activities of daily living on your own (think bathing, dressing or eating).

Since your regular health insurance won’t cover these costs—and Medicare only kicks in for hospitalizations and short-term rehabilitative care—long-term care insurance is a must. Also, Medicaid (the government program for low-income people) only covers certain long-term care expenses, and not for very long. No matter how you slice it, y’all, these options shouldn’t be your first choice.

Where Can You Receive Long-Term Care?

Figuring out where you get long-term care can be confusing—there are so many different places you can receive some sort of medical care! But there are specific facilities that give long-term care and others that don’t. Nursing homes provide long-term care. Skilled nursing facilities are often housed in the same building as nursing homes, but while they provide rehabilitation, they don’t give long-term care.

So, here are places you can receive long-term care:

- Nursing home: A facility where you live and receive the highest level of care, including help with daily living activities and usually a lot of medical care.

- Your own home: Instead of going somewhere, the caregivers come to you.

- Residential care home: Very similar to an assisted living facility but on a smaller scale, with a caregiver assigned to only three or four residents.

- Assisted living facility: A permanent place to live with other adults who need help with daily activities.

- Adult day care center: You go here to receive care during the day but return home at night.

Long-Term Care Costs Without Insurance

If you don’t have long-term care insurance in place, get ready to pay a lot of money for long-term care. It’s expensive! Let’s look at the numbers.

The estimated average cost for a semi-private nursing home stay in the United States in 2024 is $8,641 for just one month. And that number rises to $9,872 for a private room.2 Remember, that’s per month!

For a 65-year-old American today, the government estimates the average cost for LTC in their future is $120,900. But that doesn’t represent all the care that person will need. They’ll receive another $204,000 worth of unpaid care from their families, bringing the grand total value of care they’ll need to $324,900!3

These are huge numbers, guys!

And keep in mind, these costs are rising year over year even faster than inflation. For example, the annual cost for home health aide services has risen by an average of $1,153 each year from 2004 to 2021.4 And a private room in a nursing home for just one year? That went up by $43,220—or an average of $2,542 each year—during that same period.5

If you don’t have a solid plan, these costs could burn up your savings pretty quickly—unless you have a high enough net worth—then you may be able to self-insure.

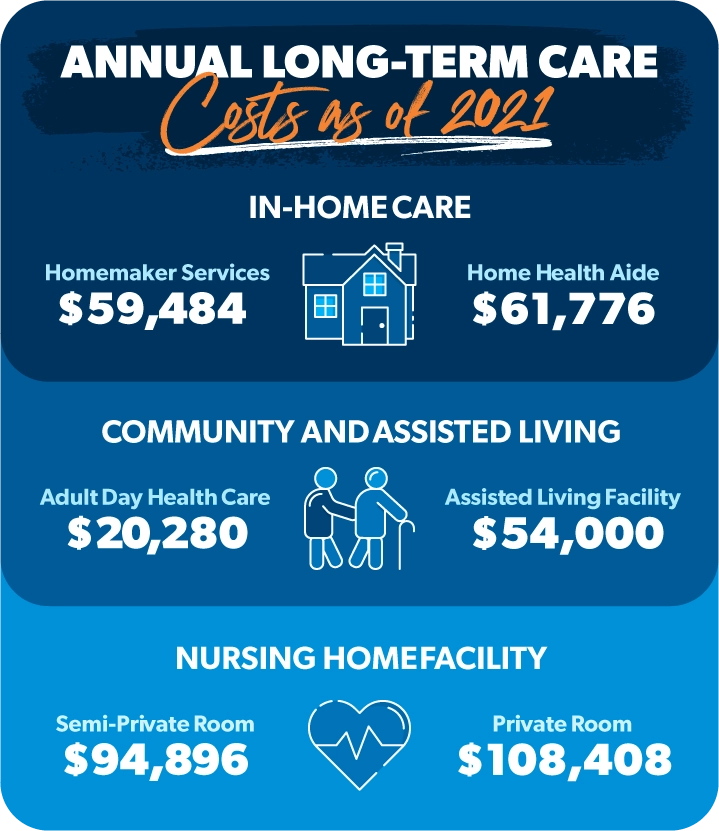

Here’s a breakdown of annual long-term care costs as of 2021.6

|

Annual Median Long-Term Care Cost as of 2021 |

|

|

Homemaker Services |

$59,484 |

|

Home Health Aide |

$61,776 |

|

Adult Day Health Care |

$20,280 |

|

Assisted Living Facility |

$54,000 |

|

Semi-Private Nursing Home Room |

$94,896 |

|

Private Nursing Home Room |

$108,408 |

How Much Does Long-Term Care Insurance Cost?

So, how much does long-term care insurance cost?

It can vary pretty widely. Yearly premiums can run as low as $1,000 to around $10,000. The insurance company will look at your age, gender, location, marital status, and current health and family health history. You’ll also pay more if you choose a longer term or a bigger benefit. And keep in mind that different carriers charge different rates for the same coverage (the #1 reason to shop around!). They can also raise your premiums after you buy the policy.

Right now, the average 60-year-old man will pay $1,200 per year for a policy that covers $165,000 in care.7 The average 60-year-old woman will pay $1,960 for the same level of coverage.8

Now ladies, don’t get upset—this isn’t a pink tax. We actually tend to live longer than men! According to federal data, women outlive men by about five years and need an average of 3.7 years of care as opposed to only 2.2 years for the average man.9,10 So it makes sense we pay more.

The good news is that couples get discounts. The average 60-year-old couple will pay $2,550 a year for a combined policy.11 Discounts are around at least 15% if you go for a couples policy.12

If you have a pretty standard policy, you’ll probably have a waiting period (also called an elimination period) between 30 and 90 days before insurance will start paying. So, keep in mind this means you should have about three months’ worth of out-of-pocket expenses ready to fill this gap, even with long-term care insurance in place.

If you’re worried about the cost of long-term care increasing and aren’t sure if your policy will cover your care, you can add something called an inflation rider. With this in place, your benefit will rise (usually around 3% per year) to get closer to inflation rates. But adding this rider also inflates your premiums to the point that it’s usually not worth it. So while it sounds like it might be a good idea, I don’t recommend it.

Factors That Affect the Cost of Long-Term Care Insurance

So, why does this stuff cost so much? And how do you keep your costs down? Well, some of it’s within your power and some of it’s not. Here are the main factors that affect the cost of LTC insurance:

- Your age: The older you are, the more likely you’ll need LTC—so you’re riskier to insure.

- Your gender: LTC insurance costs less for men than for women.

- Your marital status: Couples are more likely to care for each other rather than paying for LTC, so if you’re married, you’ll often pay less. Also, couples buying an LTC policy together can usually get a discounted rate.

- How much coverage you buy: The more apples you buy, the more you pay—same goes for insurance.

- Your health: If you’re in poor health, you’re riskier to insure.

- The benefit period you choose: If you want a longer benefit period, your premiums will be higher.

- Whether you buy inflation protection or not: Purchasing inflation protection will drive your price up.

- How long your elimination period is: Your elimination period is when you pay out-of-pocket for a set period of days before your insurance kicks in. This is like a time deductible—and the bigger your deductible, the lower your policy!

- The type of policy: Different policies have different features—and different prices.

- Which insurance company you choose: The price for LTC insurance can vary wildly from carrier to carrier.

- Where you live: The cost for LTC changes from state to state.

- Whether you qualify for a tax break: Premiums can be tax-deductible—we’ll talk about this more later.

With that many different factors, you’ll hopefully find a few ways to save money!

What’s the Cost of Long-Term Care Insurance by Age?

Let’s take a look at the annual premiums of LTC insurance by age and beneficiary:

|

Long-Term Care Insurance by Age for a $165,000 Policy Benefit |

|

|

Beneficiary |

Annual Premium |

|

55 years old |

|

|

Male |

$900 |

|

Female |

$1,500 |

|

Couple |

$2,080 |

|

60 years old |

|

|

Male |

$1,200 |

|

Female |

$1,960 |

|

Couple |

$2,550 |

|

65 years old |

|

|

Male |

$1,700 |

|

Female |

$2,700 |

|

Couple |

$3,75013 |

As you can see, premiums go up with age, so you want to figure out the right time to buy!

When Should You Sign Up for a Long-Term Care Insurance Policy?

You may be wondering, What is the best age to buy LTC insurance? I don’t think I’m going to need long-term care for a while, and I don’t want to pay premiums for something I don’t need. That’s a good point.

Then there’s the other point: Isn’t it usually cheaper to buy this kind of insurance when you’re younger? Well, you’re right about that too.

You don’t want to buy LTC insurance too early—or you’ll end up paying more in premiums than you really need to. And you don’t want to wait so long that premiums are crazy high. So there has to be a happy medium, right?

Here's A Tip

I recommend buying yourself an LTC insurance policy when you turn 60. Nothing says, “Happy birthday!” like an LTC insurance policy, am I right? Well alright, maybe golf clubs or a nice sweater sounds better. But it’ll be a happier birthday knowing you don’t have to worry about getting older! But seriously, your chances of needing LTC before age 60 are pretty slim. That’s why I recommend you buy it as soon as you turn 60.

Do Other Types of Insurance Plans Offer LTC Coverage?

There aren’t really any other ways to get long-term care insurance outside of buying LTC insurance—unless you count something called a hybrid policy.

Hybrid policies combine life insurance with long-term care coverage. They allow you to use your death benefit (the money your beneficiaries would receive when you die) while you’re still alive to pay for long-term care. If you don’t end up needing care, your heirs get the full payout.

Sounds good, right? Well, keep reading.

Are Hybrid Long-Term Care Policies Cheaper?

Some insurers decided it’d be a good idea to put LTC and whole life insurance together—a good idea for them! Not for you.

Hybrid policies are typically thousands of dollars more than traditional ones. This is because, on top of long-term care insurance, you’re also paying for life insurance you might not even need. And while hybrid policy premiums are fixed, they’re not tax-deductible.

With hybrid policies, the insurance carrier is investing your money for you, like they do with whole life insurance. The problem is, they’re choosing poor investment options and charging crazy-high fees, which means your returns will probably barely keep up with inflation. If you factor in the lost earnings compared to other investing options, hybrids might be the most expensive long-term care insurance option.

One caveat to that I’ll mention, though: If your health prevents you from qualifying for a traditional long-term care insurance policy, you might want to look into buying a hybrid plan. Even a hybrid plan is better than no plan at all.

If you qualify for a traditional policy, though, just buy long-term care insurance and life insurance separately. (And speaking of life insurance, check out my friend George’s take on why term life is your best option to protect your income and your family’s future.)

Get the long-term care insurance you need.

When a RamseyTrusted pro is in your corner, you'll have peace of mind knowing you’ve got the right long-term care insurance that won't break the bank.

Tax Benefits of Long-Term Care Insurance

So, all we’ve seen so far is how expensive long-term care insurance is. But let me tell you, there is a silver lining! LTC insurance premiums are tax-deductible up to a certain limit. And you might even be able to pay your premiums out of a pretax Health Savings Account (HSA).

How do you get these tax savings?

If you itemize your deductions, the federal government and some states allow you to count some or all of your premiums as tax-deductible medical expenses. But they must add up to a certain percentage of your income. And not all long-term care insurance plans qualify for these tax breaks. Rachel Tip: Talk to an insurance pro before you buy to make sure you get one that qualifies.

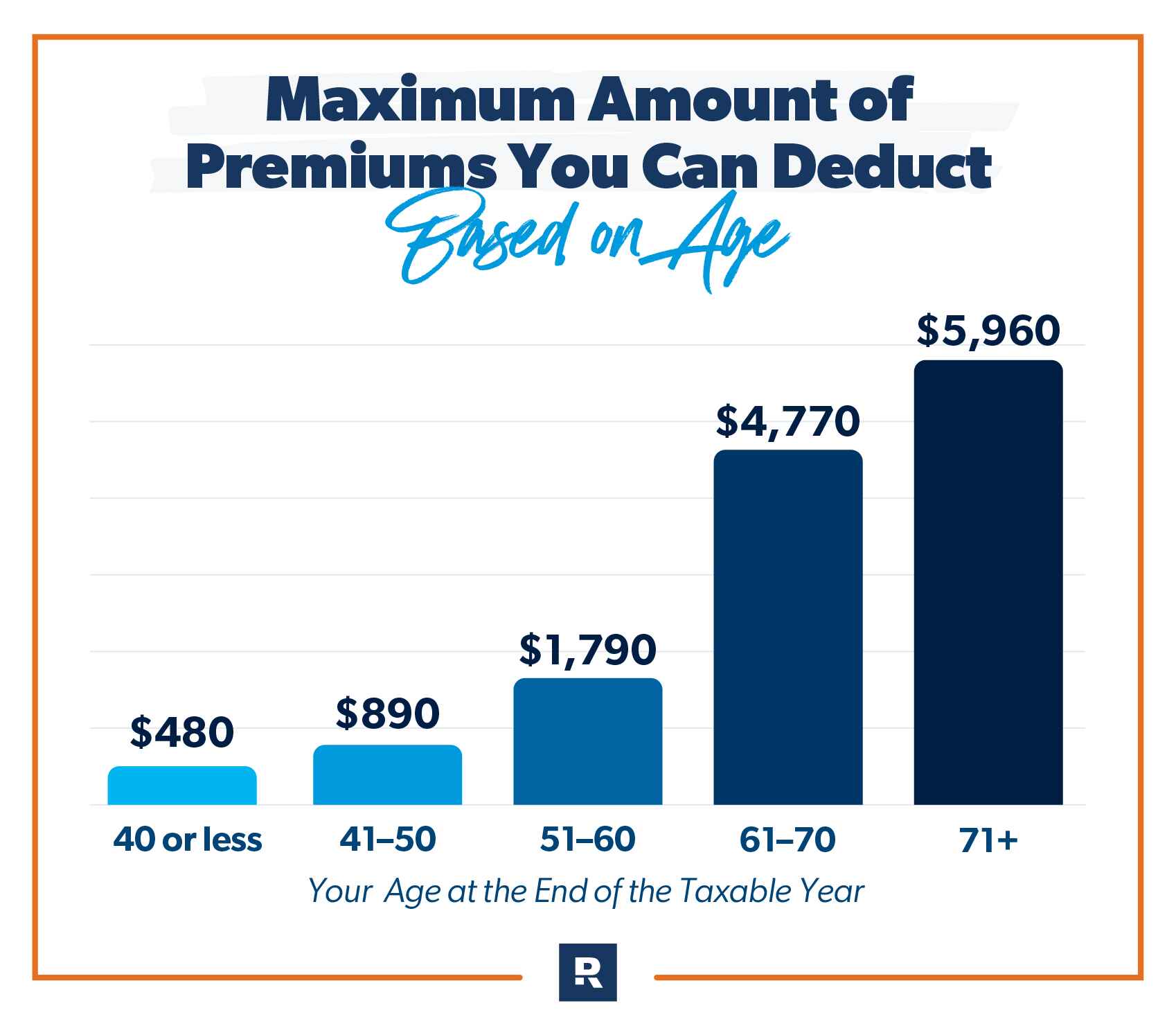

Here’s a handy breakdown from the IRS showing the maximum amount of your premiums you can deduct based on your age.14

How to Calculate Your Long-Term Care Insurance Cost

There are a few different factors to take into consideration when you’re figuring out how much long-term care insurance you need.

How much do you have saved for retirement? If you have 80 bajillion dollars in retirement, you don’t need to worry about purchasing LTC insurance because you can pay out of pocket. If you don’t have 80 bajillion dollars, consider this: Would you feel comfortable cutting a check for $250,000–300,000? Because that’s about how much you’ll need to pay for long-term care.

The second thing to consider is: What kind of care do you want? There are a few options when it comes to long-term care. These include:

- A private room in a nursing home (most expensive)

- A semi-private room in a nursing home (cheaper)

- In-home care (you get to stay in the comfort of your home!)

- An adult day care center (you go here for the day)

- An assisted living facility (people help you, but not as intensive as a nursing home)

- A residential care home (much smaller than an assisted living center)

Once you figure out what kind of care you want, you can calculate a rough cost. On average, people need about three years of care. The next step is to multiply that number by the inflation rate on long-term care, which is 3–5%.

Let’s look at an example. Chris is about to turn 60 and is looking into LTC insurance. Chris is a widower with no kids, so he’s basing his costs on a semi-private room in a nursing home.

A semi-private room at $94,896 (2021 price) for three years will cost $284,688. But Chris won’t need this room until he’s probably 80. So, calculating inflation at 4% over 22 years adds about another $250,525 to the price tag for a grand total of about $535,213.

Okay, that was a lot of math, but with this number in hand, Chris can get in touch with an insurance pro and look for a three-year policy with a benefit worth roughly $500,000 to $550,000.

Should You Get Long-Term Care Insurance?

Maybe you’re still thinking, Uh no, I’ll just keep my head right here in this hole and everything will be fine! And it might be—for a while. But check this out, guys:

Did you know that 65-year-olds today have a 70% chance of needing long-term care? And around 20% will need it for longer than five years.15 But only about 3.1% of Americans have some form of long-term care insurance.16

That’s crazy! All those folks who don’t have LTC better hope they have some really awesome kids or relatives.

And I just want to point out: The fact that you’re even reading this article means you want to be prepared. You’re already ahead of the curve, so way to go!

Having a long-term care insurance policy will take away a ton of worry about your future. It’ll also ease the burden on your loved ones. And you’ll have peace of mind knowing you won’t go broke dipping into that nest egg you’ve worked so hard for.

The last thing you want to do is pay for expensive care out-of-pocket—directly out of your savings and retirement funds. And while you could sock away a bunch of money in something like a pretax Health Savings Account (HSA), that probably isn’t the best idea since you’ll still be using up your hard-earned savings.

Long-term care insurance is a must, y’all!

How to Get Long-Term Care Insurance

So, now that you’ve learned about the costs of long-term care and long-term care insurance, maybe you’re ready to start shopping rates or to see if you qualify.

While you could do this on your own, I recommend using one of our independent and trusted insurance agents. These RamseyTrusted pros are experts in their field. They’ll shop for you so you can save time and get peace of mind knowing you’re getting the right coverage at the best price.

Are Hybrid Long-Term Care Policies Cheaper?

If you’ve been researching long-term care insurance for any length of time, you’ve probably come across something called a hybrid policy. Hybrid policies combine life insurance with long-term care coverage. They allow you to use your death benefit (the money your beneficiaries would receive when you die) while you’re still alive to pay for long-term care. If you don’t end up needing care, your heirs get the full payout.

Hybrid policies are typically thousands of dollars more than traditional ones. This is because, on top of long-term care insurance, you’re also paying for life insurance you might not even need. And while hybrid policy premiums are fixed, they’re not tax deductible.

With hybrid policies, the insurance carrier is investing your money for you, like whole life insurance. The problem is, they’re not making good investments, and your returns will probably barely keep up with inflation. If you factor in the lost earnings, hybrids might be the most expensive long-term care insurance option.

One caveat: If your health prevents you from qualifying for a traditional long-term care insurance policy, you might want to look into buying a hybrid plan.

If you qualify for a traditional policy, just buy long-term care insurance and life insurance separately. (And speaking of life insurance, learn why term life is your best option to protect your income and your family’s future.)

Tax Benefits of Long-Term Care Insurance

Although long-term care insurance is expensive, there is a silver lining: Long-term care insurance premiums are tax deductible up to a certain limit. And you might even be able to pay your premiums out of a pretax Health Savings Account (HSA).

If you itemize your deductions, the federal government and some states allow you to count some or all of your premiums as tax-deductible medical expenses. But they must rise to a certain level. And not all long-term care insurance plans qualify for these tax breaks. Be sure to ask an insurance pro to see if yours is tax qualified.

Here’s a handy breakdown from the IRS showing the maximum amount of your premiums you can deduct based on your age.19

How to Get Long-Term Care Insurance

So, now that you’ve learned about the costs of long-term care and long-term care insurance, maybe you’re ready to start shopping rates or see if you qualify.

While you could do this on your own, we recommend using one of our independent and trusted insurance agents who are part of our Endorsed Local Providers (ELP) program. They’ll shop for you so you can save time and get peace of mind knowing you’re getting the right coverage at the best price.

Next Steps

- If the cost of LTC insurance has you hesitating, read up on why it's worth it.

- Still not sure you need it? Learn more about who does.

- Get in touch with a RamseyTrusted insurance pro who can walk you through your options and get you the best deal on an LTC insurance policy.

Did you find this article helpful? Share it!

About the author

Rachel Cruze