STUDY SUMMARY

- Americans rank personal finances and money as their number one cause of significant stress.

- Thirty-four percent (34%) of Americans don’t believe they’ll recover from the financial setback of the pandemic.

- Of those who received a stimulus check in the last year, 41% used it to pay for necessities like food and bills, while 38% saved the money.

- Americans who have consumer debt are nearly twice as likely to say their personal finances have caused them to lose sleep (44%) than those who are consumer debt-free (24%).

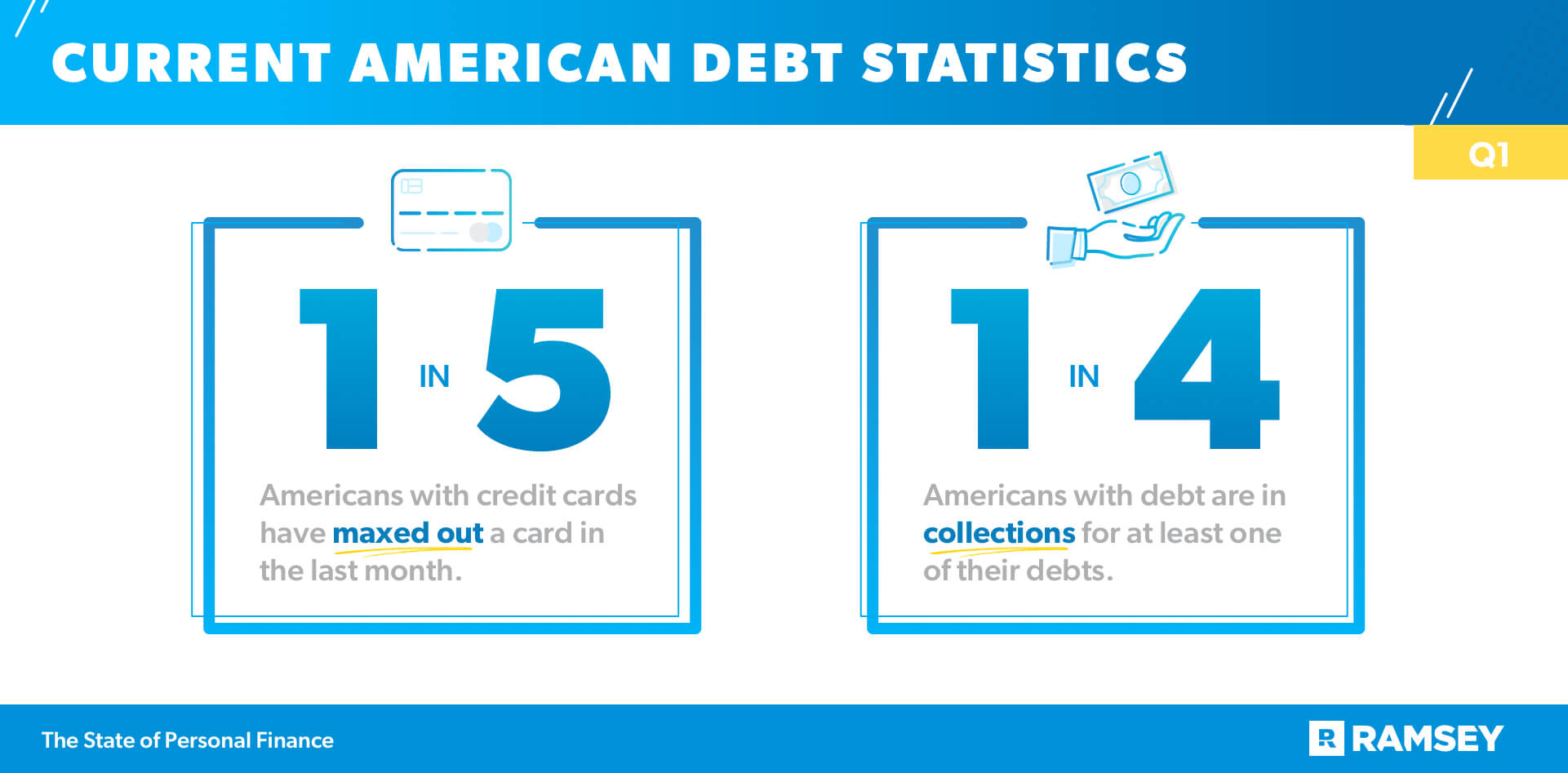

- One in five Americans with a credit card have maxed it out in the last month, and one in four Americans with debt are in collections for at least one of their debts.

- Though Americans name investing as their top financial goal, 42% are not currently saving for retirement, and over half (56%) feel behind on their retirement savings goals.

Downloads

- Research Report (PDF)

- Press Release

- Infographics

Have questions about this study? Email us or visit our newsroom for more information.

State of Personal Finance 2021 Q1

In March of 2020, America shut down in response to COVID-19, a global pandemic on a scale none of us had ever seen, and most of us had never imagined. The effects are still present in all areas of life, including finances. Thirty-four percent (34%) of Americans don’t believe they’ll recover from the financial setback of the pandemic, with those in debt more likely to doubt ever bouncing back.

Stress, worry, fear—Americans feel a range of emotions when it comes to money. In fact, they report personal finances and money as their number one cause of significant stress. Yet Americans are still forward-thinking, ranking retirement savings as their number one financial goal. And despite the past year, the majority of Americans (79%) are hopeful about their personal finances in the year ahead.

Personal Finances and Money Stress

In the last month, Americans ranked personal finances and money as the number one thing causing them significant stress. In fact, 43% of Americans worry about their finances daily, and 34% lose sleep over their personal finances. Nearly half (47%) of Americans are always worried they’ll have an emergency they can’t afford. Millennials are the most concerned here—64% of this age group reports feeling this way.

Pandemic Effects on Personal Finance

The global pandemic impacted all areas of life across the country. Money was no different. When asked to compare their current personal finances to this time last year, nearly a quarter (23%) of Americans say they are worse off.

Breaking those down demographically, we see only 19% of males and a higher 27% of females say they are financially worse off this year compared to last. Also, those who are self-employed (29%) are more likely to say their financial situation is worse than those with full-time employment (17%).

On the other end, 30% of Americans report being better off than this time last year. Of those with a graduate degree, 41% say their personal finances are better off now than last year, compared to 37% of those with a bachelor’s and 24% of those with a high school diploma or GED. Also, more Americans who say their financial situation is better now than last year are also debt-free: 42% compared to 36% who have consumer debt.

Thirty-four percent (34%) of Americans don’t believe they’ll recover from the financial setback of the pandemic. Those in debt are more likely to feel this way. Forty-two percent (42%) of Americans with consumer debt say the pandemic has been a financial setback they don’t believe they can come back from, compared to only 27% of those who are consumer debt-free.

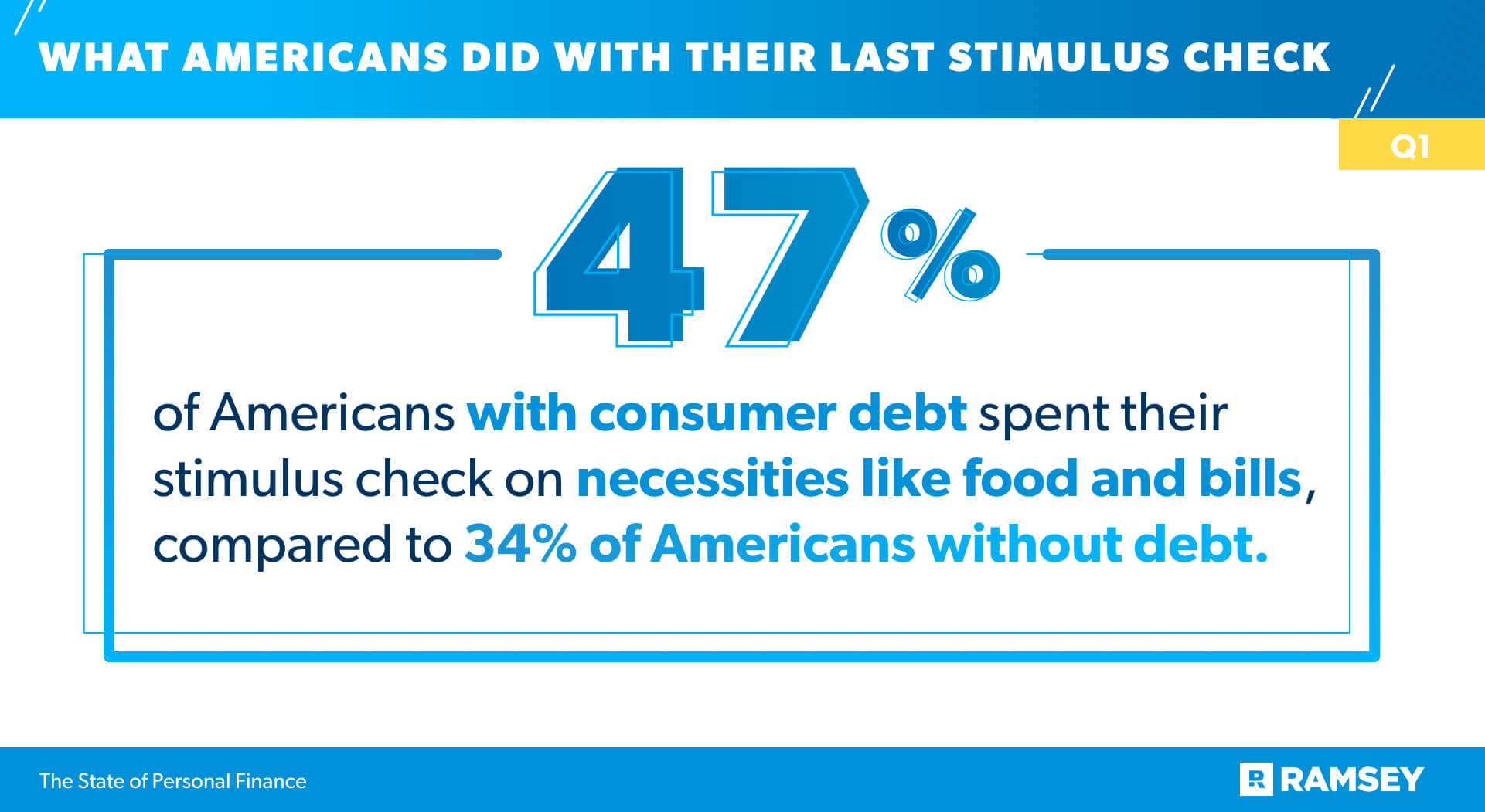

How Americans Used Their Last Stimulus Check

Of those who have received a stimulus check in the last year, 41% used it to pay for necessities like food and bills, while 38% saved the money. Those without consumer debt (45%) were more likely to save the stimulus money than those with debt (31%). On the other side, those with debt (47%) were more likely to spend the money on necessities than those who are debt-free (34%).

Current American Credit Card Statistics

Eight in 10 Americans have a credit card. Most of those have one to two cards, and half use one regularly. Among those using credit cards, four in 10 carry a balance and are racking up interest.

What’s the main motivation for using this type of debt? One in four say they use credit cards to cover expenses they can’t cover with cash. Yet despite their aim at a sense of security, one in five Americans with a credit card have maxed out a card in the last month.

The Federal Reserve reports that 77% of American households have at least some type of debt.1 Our research shows one in four Americans with debt are in collections for at least one of their debts. The generation most affected by both of these money problems? Millennials. Forty percent (40%) of millennials who have a credit card have maxed one out in the last month, and half of millennials with debt have at least one in collections.

The Emotional Effects of Debt on Americans

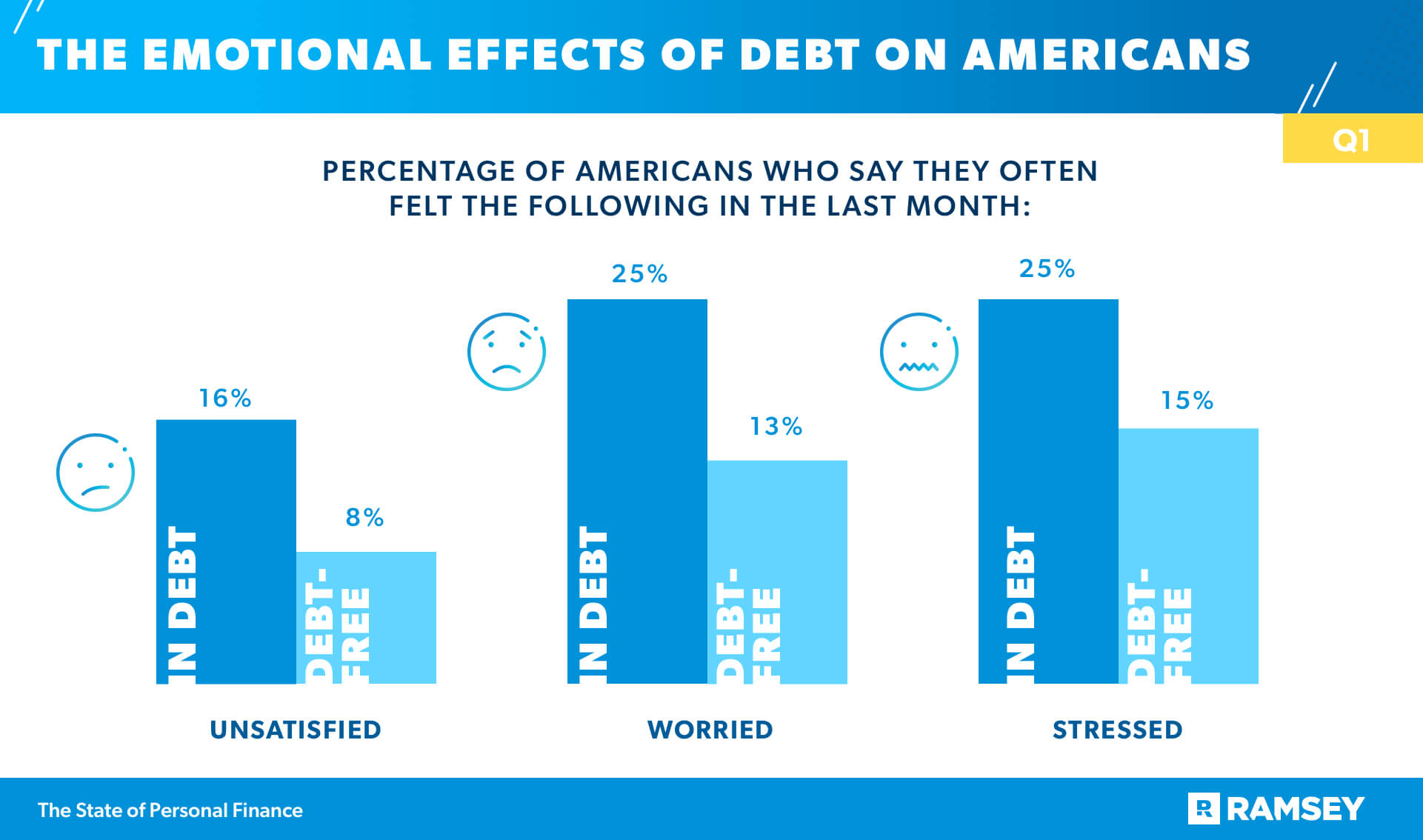

This study has already shown some effects of debt on Americans, but now we’ll look deeper into the emotional impact it can bring. Americans with consumer debt are nearly twice as likely to lose sleep because of their personal finances (44%) than those who are consumer debt-free (24%). More than half (54%) of Americans with consumer debt worry daily about their finances, compared to only one-third of Americans who are consumer debt-free.

Less than one-quarter (23%) of Americans with debt rate their mental health as great, compared to 34% of Americans who are consumer debt-free. Also, those with consumer debt are twice as likely to say they often feel unsatisfied (16% vs. 8%) as well as worried (25% vs. 13%). They’re also more likely to say they often feel stressed (25% vs. 15%).

Personal Finance and Student Loan Debt

Intended as a tool to provide better and further career opportunities, student loans often lead to a sense of regret and feeling stuck. Over half (53%) of those who took out student loans to pay for school say they regret doing so. In an even more striking find, 43% of those who took out student loans regret going to college altogether.

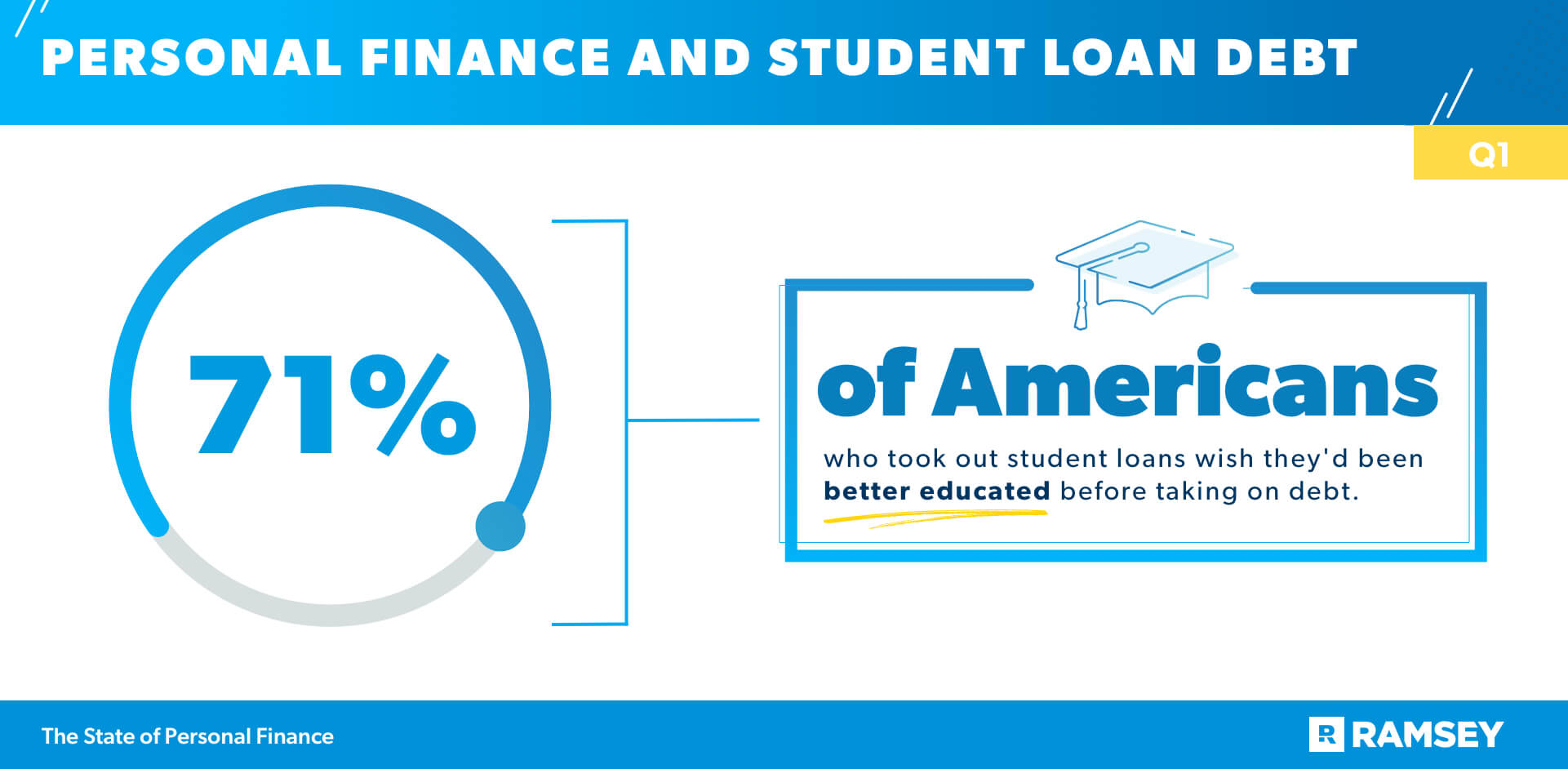

Those we surveyed feel ill-informed on alternative options to covering college costs. In fact, 71% of those who took out student loans to pay for school say they wish they’d been better educated about debt before taking it on.

Many Americans feel held back by the burden of their student loans. Nearly half (47%) of those who used student loans to pay for school say they’ve delayed other things they want to do in their lives—such as buying a home, getting married, or having a child—because of their student loan debt.

Budgeting Habits in America

After a year of intense financial stress and uncertainty, six in 10 Americans still don’t create a monthly budget to manage their finances. However, of the 40% who are budgeting, more than one-third just started budgeting in the last year. Why do Americans begin budgeting in general? Many reasons, including wanting to increase savings and wealth (26%), wanting to get their spending under control (21%), and wanting to pay off debt (17%).

Budgeting has benefits beyond financial management. Budgeters are more likely to say they often feel hopeful (44%) compared to those who don’t budget (34%). Also, 64% of monthly budgeters are currently saving for retirement, compared to only 52% of those who don’t budget.

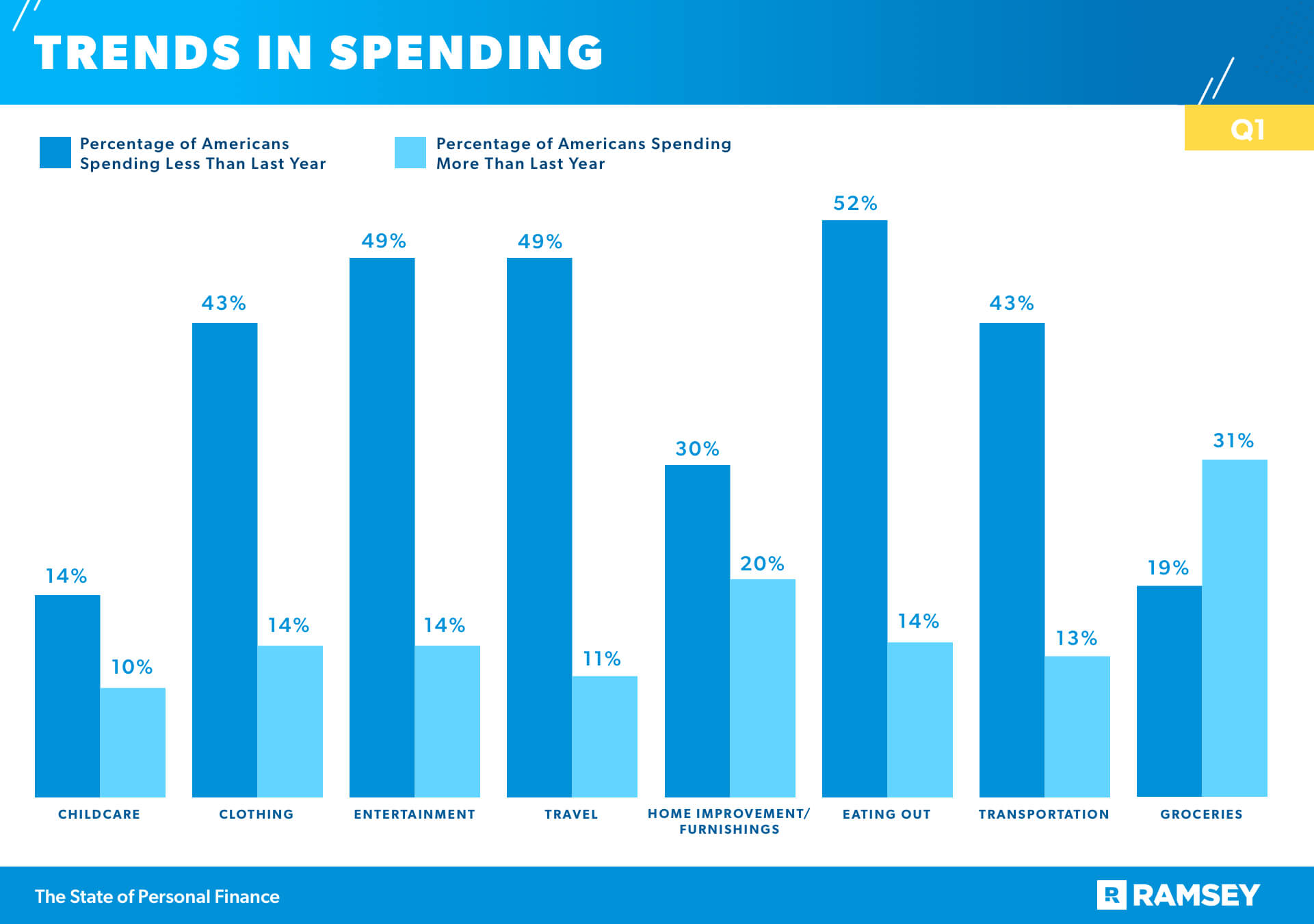

Pandemic Trends in Spending

As a result of COVID, 22% of Americans cut out expenses to save money, 14% started saving for emergencies, and 13% delayed a major expense they’d planned.

What do current spending trends look like? Overall, Americans are spending less than last year across several major budget categories. More than half (52%) of Americans are spending less on eating out, 49% are spending less on entertainment, and 49% are spending less on travel. Groceries is the only category where the spending trend went up more than down. Thirty-one percent (31%) of Americans say they spent more last year on groceries, while only 19% said they spent less.

Retirement and Investment Trends

The top two financial goals Americans have are related to short-term and long-term savings, with retirement ranking as number one.

Top Two Financial Goals

#1 Save for Retirement

#2 Save More Money in the Bank

Though investing is a top goal, 42% of Americans aren’t currently saving for retirement, and over half (56%) of Americans feel behind on their retirement savings goals. Across generations, the percentage of those saving for retirement is fairly close: 60% of millennials, 61% of Gen X, and 59% of baby boomers. Those with a graduate degree are the most likely to be currently saving for retirement (75%), as are those with a household income of $100K+ (80%). In fact, only 33% of those with a household income under $55K are saving for retirement.

Another notable discrepancy in retirement savings is across gender: 63% of males and 50% of females are saving for retirement.

Despite the buzz, very few people are putting money into these newer, unproven investment vehicles like cryptocurrency and NFTs (nonfungible tokens). In fact, only 4% have invested in cryptocurrency and 1% in NFTs.

Personal Finances and Hope for the Future

The year behind us brought setbacks, stress and instability. However, in the last month, 45% of Americans say they’ve often felt grateful, and 43% say they’ve often felt happiness. Though they may currently feel held back by their financial situation, eight in 10 Americans with debt do believe they can become debt-free.

Seven in 10 Americans say the ability to win with money is within their control—that it is more dependent on their personal habits rather than their external circumstances. And nearly eight out of 10 Americans (79%) are hopeful about their personal finances in the year ahead. This indicates most Americans have hope in their financial future and believe their habits and actions will be what brings the results they need with money.

About the Study

The State of Personal Finance Study is a quarterly research study conducted by Ramsey Solutions with 1,023 U.S. adults to gain an understanding of the personal finance behaviors and attitudes of Americans. The nationally representative sample was fielded March 25, 2021, to March 30, 2021, using a third-party research panel.

Did you find this article helpful? Share it!

About the author

Ramsey Solutions