The toxic debt culture is stealing your income, and that’s not okay. Learn how to take charge of your future and become debt-free.

The Truth About Debt

-

Don't Buy Into the Myth

"Debt is a tool for building wealth." Wrong! Your income is your greatest asset. But if debt owns your paycheck, you’re paying for the past instead of building your future.

-

Normal Is Broke

“Buy now, pay later” might feel normal, but normal will keep you in a never-ending cycle of money stress. If normal is broke (and it is), then it's time to get weird.

-

There’s a Way out of Debt

Personal finance is 80% behavior and 20% head knowledge. And with the right plan in place, you’ll make your bad money habits and debt disappear for good.

-

You Can Live a Debt-Free Life

Imagine a life with no debt payments and the freedom to save, give and build wealth. It’s possible! And the debt snowball will help you get there.

How the Debt Snowball Method Works

Step 1

List your debts from smallest to largest (regardless of interest rate).

Step 2

Make minimum payments on all your debts except the smallest debt.

Step 3

Throw as much money as you can on your smallest debt every month.

Step 4

Once it’s paid off, add that payment to the next-smallest debt.

Step 5

Repeat until each debt is paid in full and you’re completely debt-free.

See How Simple Budgeting Can Be

Budget Calculator

Enter your income and the calculator will show the national averages for most budget categories as a starting point. A few of these are recommendations (like giving). Most just reflect average spending (like debt). Don't have debt? Yay! Move that money to your current money goal.

Income

Expenses

Difference

$0.00

Total Expenses

$0.00Watch Your Small Money Wins Turn Into Unstoppable Momentum!

In the first month, most EveryDollar budgeters . . .

-

Uncover up to $395 to use toward debt

-

Cut monthly expenses by 9%

-

Build better budgeting habits

You work too hard to let debt rob you of the life you’re meant to live. It’s time to take control of your money and pay off your debt for good!

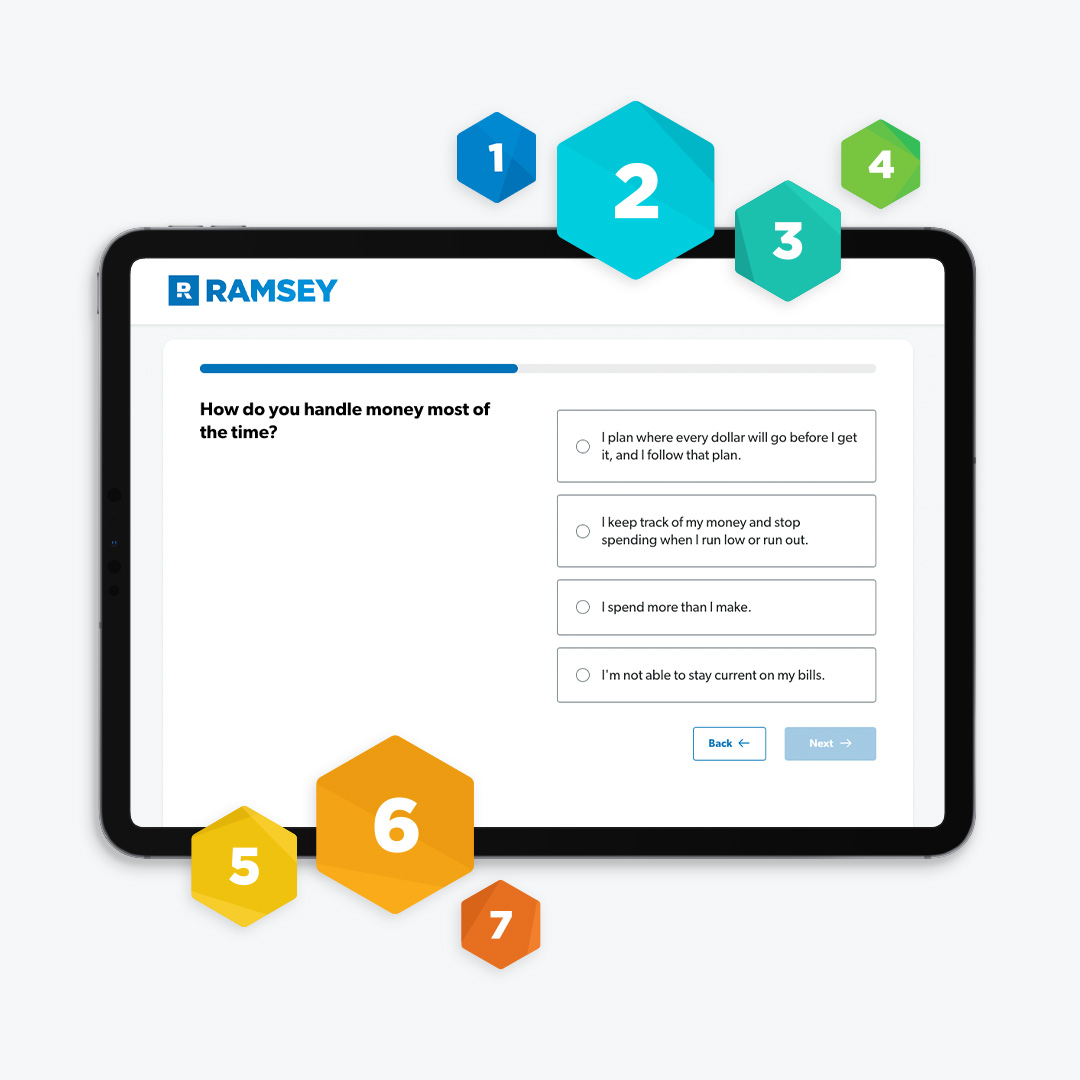

Not Ready to Budget Yet?

Answer a few questions, and we’ll set you up with a plan that meets you where you are right now.

Share a little about yourself—like your life and money goals.

Dive into your results to see your step-by-step action plan.

Your money goals can be achieved, and we’ll guide you.

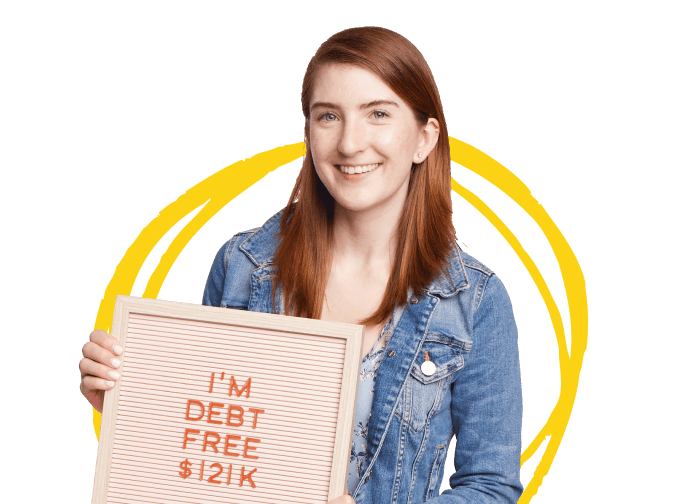

Yes, You Can Do This

"I paid off $121,000 in 28

months. I feel strong! The

burden is gone!"

“We're not stressed anymore. Our journey's in our hands now. We get to choose what we want to do."

"There’s freedom on the other side of debt. You don’t have to live like everyone else. I wanted something different for my family."

Free Tools to Help You Pay Off Debt Fast

Common Questions About Debt

-

Why do I pay off my debt starting with the lowest balance instead of the highest interest rate?

-

The debt snowball is all about motivation. By paying off your smallest debt first, you get a quick win! Plus, you immediately free up money to tackle the rest of your debt. The debt snowball creates unstoppable momentum to knock out the rest of your debts—like a snowball rolling down a hill! Learn more about how to pay off debt.

-

Which debt should I pay off first?

-

If you’ve got multiple debts, pay off the smallest debt first (regardless of interest rate). But if you owe the IRS any money (aka tax debt), you need to take care of that before anything else—even if it isn't your smallest debt. Get your top debt snowball questions answered.

-

Should I pay off debt before I save for retirement?

-

Around here, we teach the 7 Baby Steps. If you’ve got any debt (other than your mortgage), your goal is to pay it all off before you start saving for your future—and that includes investing for retirement. Trust us, the best thing you can do for your financial future is ditch your debt so you can free up your income and start building wealth faster. Find out how to start.

-

How do I get out of credit card debt?

-

The debt snowball method is the best way to get rid of credit card debt. But you also need to stop using credit cards (cut those suckers up!), get on a budget, control your spending, and do whatever you can to pay off your credit cards ASAP. Also, avoid things like balance transfers, personal loans and more credit cards—those will only make your problem way worse.

-

How do I handle debt collectors?

-

Debt collectors have one mission and one mission only—to get your money. And they’re not above stooping to some pretty low levels to make you pay (like lying, harassing and manipulating you). But you have rights, and you can defend yourself against these bullies! Find out how to deal with debt collectors.

-

Should I file for bankruptcy?

-

Bankruptcy is a gut-wrenching experience that lays out your money problems for all to see and drags you through the legal mud. It also stays on your credit report for years and doesn’t even erase all your debts in most cases. You should do everything in your power to avoid filing for bankruptcy. Get the truth about bankruptcy.