Introduction

A new year is always full of potential—a second chance, an opportunity to turn over a new leaf and change old habits. Losing weight, thinking more positively, reconnecting with friends and family, and getting ahead in your career are all great goals for a new year. But the one New Year’s resolution that many Americans are looking to keep is saving money.

And that makes sense. With wise money management, you’re not living paycheck to paycheck and constantly stressing about money, and that brings a feeling of peace. You can enjoy the freedom that comes with living the life you want—comfortably weathering the storms of life, preparing for the future, and giving to the people and causes you want to support.

In this year-end edition of The State of Personal Finance report, we’re analyzing some of the ways Americans are trying to get ahead with money in 2025. Some are great steps to take, others could be missteps, while still others are just plain odd.

Executive Summary

- Saving money was the top New Year’s resolution for Americans.

- 37% of Americans said their personal finances will get better during the second Trump presidency.

- 1 in 4 U.S. adults plan to use their tax refund to treat themselves—whether it be travel, clothes, eating out or something more.

- Grocery shopping was the number one budget category where Americans said they’re most likely to overspend.

- Nearly 6 in 10 American adults said weekly meal planning is an essential task, but 44% wish they were better at it.

- Americans said the ideal interest rate for them to consider buying a home in the next 12 months is 4.5%.

- 45% of Gen Z and millennials said if the government increased the child tax credit, it would have a big or moderate impact on their decision to have a child or additional children.

- About half of Americans have given money to a person in need or a charitable cause in the last three months.

- 33% of Americans said it’s acceptable to borrow money from the person you’re dating to pay a bill.

Download a PDF version of the report.

Americans Are Looking Forward to Saving in the New Year

Every new year, Americans resolve to get better at managing money in some way. In 2025, they’ve put saving money at the top of the list.

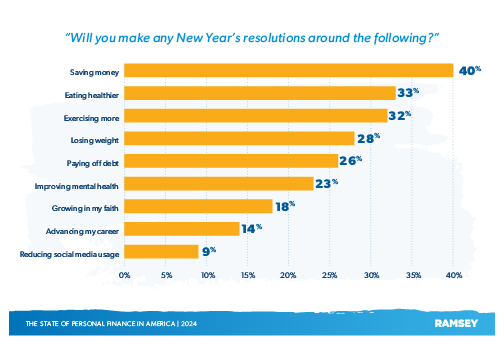

Saving money was the most common New Year’s resolution for 2025, with 40% of U.S. adults saying they’re making savings a priority. This significantly beat out eating healthier (33%), exercising more (32%) and losing weight (28%).

And although young people have often been stereotyped as irresponsible, just living for today, and not very concerned about their future—which includes saving money—the young may be bucking that convention, as Gen Z is the generation with the most potential savers (57%). Baby boomers, who are now retiring, were the generation least likely to make saving money a resolution (27%).

In fact, for baby boomers, saving money was almost tied with exercising more (28%) and eating healthier (28%). But that’s to be expected, as most baby boomers have some savings (69% of them have over $1,000 in savings according to a previous edition of our State of Personal Finance survey) and are instead more concerned with keeping better tabs on their health as they age.

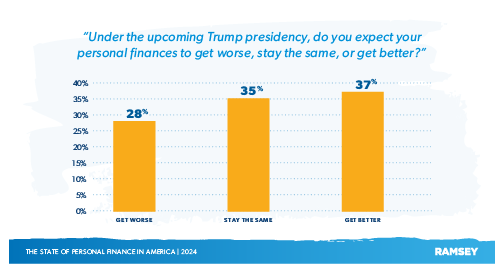

Adding to the renewed enthusiasm for saving money may be the reelection of President Donald Trump. As mentioned in the previous quarter’s State of Personal Finance report, about half of Americans believe the president has a major impact on their personal finances. When asked specifically about the incoming Trump administration for this report, more Americans did think their personal finances would get better under Trump than worse (37% vs. 28%). However, almost as many Americans believed their financial situation would stay the same (35%) as those who expected an improvement.

Regardless of who is In the White House, changing your own behavior is the key to making real improvements in your life—whether it be losing weight or saving money.

Despite the desire to save more, many Americans have a habit of spending any extra money that comes their way. Many adults look at tax refunds as free spending money (even though it’s actually your money the government borrowed from you interest-free). In fact, 1 in 4 U.S. adults (27%) plan to use their 2024 tax refund to treat themselves—whether that’s travel, clothes, eating out or something else. That’s 70 million Americans.

Millennials were the most likely to spend a tax refund (37%) and baby boomers were the least likely (15%). However, a quarter of Americans (26%) aren’t going to spend (and will hopefully save) their refund, while the rest (47%) aren’t expecting a refund at all.

Curbing the Cost of Food Is Essential for Saving Money

Food is one of the largest portions of any household budget. We need it to survive, and we all have those favorites we like to indulge in. Whether it’s due to impulse buys or not making shopping lists, people often struggle to keep a lid on their food budget. And the rise in costs brought on by inflation in the last few years hasn’t made the situation any better.

In order to dial up their savings game, Americans need to get a handle on food spending—and they can. Through intentional planning, people can find that margin to put away money for a rainy day.

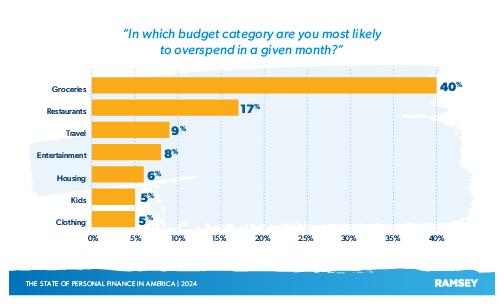

Overall, grocery shopping is now the number one budget category where Americans are most likely to overspend—greatly outpacing even restaurants and travel.

And it looks like we can’t even blame the kids (though it may sometimes feel like they eat you out of house and home). The data suggests that just as many people with children under age 18 in the house overspend on groceries (40%) as those who don’t have kids (39%). And baby boomers, who are mostly empty nesters, were more likely to overspend on groceries than the younger generations, sitting at 44%.

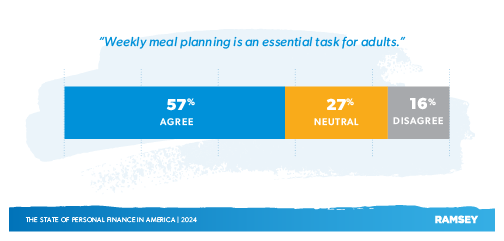

With most American households (72%) going grocery shopping at least once a week, planning out meals weekly has become a popular way to curb the cost of food. It helps you know exactly what to buy and be less susceptible to uncertainty and impulse purchases. Nearly 6 in 10 U.S. adults said weekly meal planning is an essential, with a higher percentage of married adults finding it important than singles who never married (64% vs. 48%).

Americans may say that meal planning is essential, but many aren’t very confident in their abilities. Almost half of Americans (44%) wish they were better at meal planning. This is especially true of the younger generations, with Gen Z being the most likely to say they want to be better at meal planning (58%). The feeling is also fairly even across annual household income levels (44% on average, no matter the household income).

Americans Are Putting Off Big Decisions to Save Money

Another way Americans are looking to save money is by simply delaying major expenses, which they think will mean the difference between hundreds, if not thousands, of dollars. People are waiting for the right time and opportunity to take big leaps—even though that “right time” may never come.

Buying a home is one of those big leaps, and the market’s volatility over the last five years has prompted many potential homeowners to stay on the sidelines and wait for mortgage interest rates to lower to where they were prior to 2020. When asked, Americans said 4.5% is the “magic number” for mortgage rates for them to consider buying a home in the next 12 months. Rates currently stand at 6.27% for 15- year fixed-rate mortgages (which are usually about one percentage point lower than 30-year fixed-rate mortgages).1

While rates are expected to go down even more in 2025, people may also have to lower their expectations if they want to enter the market.

And here’s another big decision Americans are putting off: having kids. Raising children is a rewarding experience, but it requires a lot of love, patience and sacrifice from parents. It’s an even larger sacrifice today, as the USDA estimated that a child born in 2015 would cost around $233,000 to raise from birth to age 18, which is over $300,000 in 2024 dollars.2 According to demographic experts, the cost of raising children is a factor in the declining number of births in the United States, which is now at its lowest since 1979.3 Many Americans are delaying having children until they’re in a more economically sound position—working a well-paying job and able to save money.

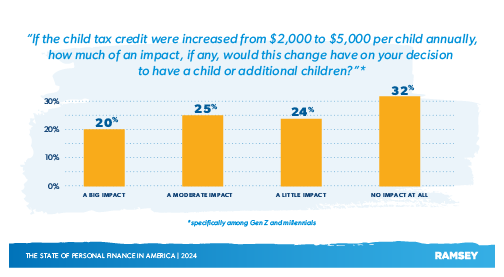

So, potential parents are looking for any break they can get to make the child-raising journey a little easier. According to the data, 45% of Gen Z and millennial respondents (the generations most likely to become parents) said that if the government increased the child tax credit, it would have a big or moderate impact on their decision to have a child or additional children.

Giving Is Good—Lending, Not So Much

It may sound counterintuitive, but one of the great things about saving money and building wealth is being able to give it away. Outrageous generosity is a virtue that brings as much satisfaction to the giver as it does to the receiver. You could make someone’s day, week, month or year by giving a big tip on a restaurant bill or handing someone a check to pay for a big expense. When our cup runs over and we’re free from payments, the possibilities are limited only by our sense of generosity.

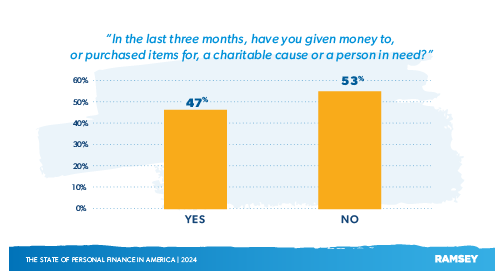

However, it looks like many Americans aren’t feeling very generous lately. In the last three months, only about half of Americans (47%) have given money to, or purchased items for, a charitable cause or a person in need.

At first glance, this may reflect poorly on America’s sense of generosity. But keep in mind that a huge majority of the country (77% according to the latest statistics) is shouldering some kind of debt, which makes both saving and giving extremely difficult.4 But despite that, overall, America is one of the most generous nations in the world.5

Income is also a factor in giving for Americans, as is religious participation. People making over $100,000 a year were more likely to give than those making under $50,000 (63% vs. 33%). And 65% of those who have attended religious services recently said they gave money compared to only 40% of those who haven’t.

While giving is good for the soul, borrowing or lending isn’t—especially if you’re lending money to someone close to you.

It’s even more awkward to lend money to someone you’re dating. Yet, one-third of Americans (33%) said it’s acceptable to borrow money from the person you’re dating to pay a bill. Younger people were more open to the idea, with 55% of Gen Z saying borrowing from a boyfriend/girlfriend is acceptable, compared to just 13% of baby boomers. And singles who had never been married were more likely to agree than married people (40% vs. 27%). In every situation, it’s better to just give the person money (if you’re able) rather than have a debt hang over your relationship.

Conclusion

The state of personal finance in America is somewhat hopeful. People seem to be looking forward to 2025 with a renewed sense of purpose, wanting to take control of their finances and save money. Saving will be essential to building wealth in 2025, but if we’re not careful, our old habits and behaviors can slow down any progress we hope to make.

The truth is, it’s not up to how much you make or whoever’s in the White House. The key to saving is focused, consistent behavior change—such as living below your means, avoiding debt, building an emergency fund, and saving for retirement. The highs brought about by living and spending in the now are temporary, but smart saving behaviors can last a lifetime.

The best part is, once you’ve established those saving behaviors, you’ll have the peace of knowing that you’re prepared for whatever life throws at you—instead of living one paycheck away from complete disaster. And as a bonus, you’ll be in a great position to change someone else’s life through giving. Just make sure you’re actually giving and not lending money—it’s more fun that way.

About the Study

The State of Personal Finance is a quarterly research study conducted by Ramsey Solutions with 1,032 U.S. adults to gain an understanding of the personal finance behaviors and attitudes of Americans. The nationally representative sample was fielded December 3–10, 2024, using a third-party research panel. Margin of error was ±3.05%.

Since January 2021, The State of Personal Finance study has surveyed over 15,000 U.S. adults. Research from the study has been shared on hundreds of media outlets, ranging from Forbes to Fox News Channel to The New York Times to Good Morning America, as well as in ad campaigns during the NBC coverage of the 2024 Summer Olympics in Paris.

Did you find this article helpful? Share it!

About the author

Ramsey Solutions